How it Works: Mortgage Partnership Finance® (MPF®) Program

Caroline Casavant

The Mortgage Partnership Finance® (MPF®) Program supports FHLBank Boston members in extending housing financing to their communities. MPF allows members to access liquidity, tailor risk, and focus on their competitive advantage: credit risk in their communities.

MPF and the Federal Home Loan Bank (FHLBank) System’s Housing Affordability Mission

Congress created the FHLBank System to provide reliable liquidity to its member institutions and support housing finance and community investment. Along with advances and letters of credit, FHLBank Boston provides its members with liquidity through the MPF Program.

Member institutions have unique insights into their customers’ credit profiles and communities’ housing finance needs. Participation in the MPF Program allows member institutions to focus on these unique competitive advantages by offloading interest-rate risk, prepayment risk, and some credit risk to FHLBank Boston. The ability to offload these risks and improve balance sheet liquidity improves the availability of housing financing to local communities.

MPF Program Overview

To participate in the MPF Program, FHLBank Boston members must be approved to become a Participating Financial Institution (PFI). The dedicated MPF team at FHLBank Boston, led by Jennifer Cowles, is available to assist member institutions with applying to become PFIs.

Once documentation is established, PFIs can sell mortgage loans they’ve originated to FHLBank Boston in exchange for liquidity, which is received as funds same day or the next business day. Loan sales are pooled into a Master Commitment, which defines the amount of loans a PFI may sell over a specific period. The minimum size of a Master Commitment is $5 million. Commitment to deliver loans may occur on a mandatory basis, where the committed dollar amount must be delivered, or on a “Best Efforts” basis, where the PFI is required to deliver a specific loan only if the loan ultimately closes.

Eligible mortgage loans must be fixed rate, fully amortizing, and within agency-conforming loan limits, or high-balance loan amounts, and all property types are accepted except co-ops and investment properties. There are no further loan-level price adjustments.

The MPF Program is intended to integrate well with common automated underwriting systems, like:

- Fannie Mae® Desktop Underwriter® or Freddie Mac Loan Product Advisor®

- Manually underwritten mortgage loans

Typically, when a PFI sells a mortgage loan to FHLBank Boston, the PFI could retain servicing rights, so it remains the primary point of contact for its local customer. The PFI will receive compensation for servicing these loans by retaining 25 basis points as a servicing fee. Alternatively, they can sell the servicing rights to an MPF-approved provider or use a sub-servicer.

Here’s what then happens to each component of the underlying risks in the mortgage once sold to FHLBank Boston:

| Interest-rate | Transferred to FHLBank Boston |

| Liquidity | Transferred to FHLBank Boston |

| Credit | Shared with FHLBank Boston & PFI |

Sharing of Underlying Credit Risk

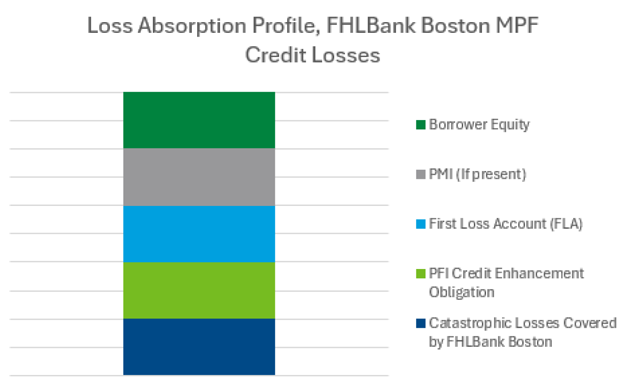

When a PFI sells a mortgage loan, the credit risk in that loan is shared between the PFI and FHLBank Boston.

When a PFI sells a mortgage loan, the credit risk in that loan is shared between the PFI and FHLBank Boston. The bulleted list below outlines a typical loss structure for a loan sold to MPF. Here’s how the tranches are structured:

- First tranche: Equity in the mortgage loan. This reflects the value of the property less the amount of the loan.

- Second tranche: Private Mortgage Insurance (PMI). This protects the lender if a loan defaults and there is a loss.

- Third tranche: First Loss Account (FLA) owned by FHLBank Boston. The First Loss Account equals 35 basis points of the principal balance of mortgage loans sold by a PFI to FHLBank Boston. It is designed and expected to cover normal credit losses and has done so historically.

- Fourth Tranche: Credit Enhancement (CE) Obligation provided by the PFI. The CE obligation varies depending on the individual credit risks associated with the loans sold. The MPF team is available to help PFIs determine the specific CE obligations associated with any pool of underlying loans ex ante. The CE obligation is collateralized by loans pledged to FHLBank Boston. The total of the FLA and CE obligation is subject to a pool minimum of 1.00% and is subject to a pool true-up to a secondary model.

- Fifth Tranche: FHLBank Boston loss. Any losses that exceed the first four tranches will be absorbed by FHLBank Boston, which allows PFIs to identify their maximum potential loss with each Master Commitment.

Importantly, because the PFI retains some credit risk in the underlying loan, the PFI is compensated through a monthly payment from FHLBank Boston, called “Credit Enhancement income,” part of which is tied to loan performance. Credit Enhancement income is recouped; there is a loss that hits the FLA.

Strategic Benefits of Utilizing MPF

Participation in MPF provides several advantages for PFIs. Among these benefits:

- Improved Liquidity Profile. PFIs can convert eligible loans to liquidity by selling them to MPF and receiving cash the day after the loans are sold. In so doing, they free up room on their balance sheets to pursue alternative lending opportunities or better meet liquidity and cash needs.

- Ability to Reduce Interest-Rate and Convexity Risk. When a loan is sold to MPF, FHLBank Boston incurs risks associated with interest rates and prepayment. This means that the PFI is no longer responsible for monitoring or otherwise hedging these risks. They can instead focus on their own competitive advantage, like knowledge of local credit markets.

- Enhanced Earnings Compared to Other Secondary-Market Options. When PFIs sell eligible loans to the MPF Program, they retain some of the credit risk and are compensated for doing so. Thus, PFIs continue to see upside from loans that perform well in the form of regular payments associated with those loans. This differentiates MPF from other secondary-market options.

- Preservation of Borrower Relationships. FHLBank Boston allows PFIs to retain servicing rights, should they choose to do so. The PFI is therefore able to remain the primary point of contact with its local customers and support its community members while building relationships that may be value accretive over time.

- Improved Ability to Respond to Market Conditions Changes. Participation in the MPF Program as a PFI allows member institutions to quickly change their overall exposure to mortgage loans. This makes them more nimble in different environments. For example, if a member institution wants more room on its balance sheet to issue new mortgage loans at a higher rate after a period of rising interest rates, it can do so by selling lower-rate loans to MPF. Similarly, should a member wish to reduce its overall exposure to loans to serve its community through a different loan vehicle, it can similarly sell to MPF to reduce its footprint in mortgage loan markets.

MPF Program Participation Compared to Alternatives

A common secondary-market alternative to MPF participation is selling loans to Fannie Mae or Freddie Mac. Small member institutions or those that have limited mortgage loan origination for strategic reasons may find PFI participation and access to MPF to be operationally easier or more cost effective.

Competitive advantages of the MPF Program include:

- No loan-level price adjustments

- Transfer of servicing not required

- Receive compensation for loan performance

- Maintain borrower relationships

- Additional loan types may be eligible for sale

- Operationally easy and cost effective

Risks and Considerations

MPF participation allows a PFI to tailor the risk associated with its mortgage loan exposure, but it does not eliminate risk. It’s important to note that PFIs retain some credit risk on the loans they sell to MPF, and they must manage their risk in a way that accounts for the possibility of losing their CE obligation.

Because PFIs pass interest-rate and prepayment risks associated with a loan to FHLBank Boston when they participate in the MPF Program, they will no longer incur losses from managing these risks.

Finally, PFIs must comply with MPF Program guidelines, servicing standards, and reporting obligations.

Regulatory and Accounting Considerations

PFIs retain responsibility for record keeping and accounting related to participation in the MPF Program. In general, when a PFI participates in MPF, the institution must then value:

- Mortgage loan servicing rights

- CE income, and the expected value of those payments

- Potential loss of the CE Obligation should the FLA be depleted

- Difference between a Mandatory Commitment and a “Best Efforts” commitment.

Case Studies Regarding Potential Credit Loss Outcomes

Let’s look at some hypothetical examples of how the MPF process works in different scenarios. The three case studies below highlight how the loss absorption profile works in practice.

Case Study One: Credit Loss Occurs, But Affects Only FHLBank Boston

A PFI located in New Hampshire called “Live Free and Refinance Bank” sold $10,000,000 mortgage loans to FHLBank Boston. The CE obligation associated with Live Free was 5%, or $500,000. The FLA posted by FHLBank Boston is 35 basis points of the unpaid principal balance of the sold loans, or $35,000. The actual amount posted to the CE obligation equals the CE minus the FLA ($500,000 – $35,000 = $465,000).

After the Master Commitment (MC) closes, one of the borrowers (of a loan sold into the MC) experiences material economic distress following a legal dispute over whether Manchester truly invented chicken tenders, and he stops making mortgage loan payments, and the home is foreclosed upon. There is no equity in the home, nor does the loan have PMI, and as a result, there is a loss that totals $15,000.

The impact:

Since there is no equity or mortgage insurance to cover the loss on the loans, the third tranche will absorb the loss, and FHLBank Boston will post the FLA. The value of the FLA account was $35,000, and in covering the loss, the value of the account will be depleted by $15,000 to $20,000. The CE obligation is not affected by this loss, though. FHLBank Boston will recoup future performance-based CE income from Live Free to make up for the loss to the FLA.

| Borrower Equity | Negative, no equity available |

|---|---|

| PMI | No PMI available |

| First Loss Account | $35k available to absorb losses, $20k remains |

| PFI CE Obligation | No losses |

Case Study Two: Credit Loss Occurs and Impacts Both FHLBank Boston and the PFI

A PFI in Maine called “Wicked Good Mortgages” sold $10,000,000 mortgage loans to FHLBank Boston. The CE obligation was 5%, or $500,000. The FLA posted by FHLBank Boston is 35 basis points of the unpaid principal balance of the sold loans, or $35,000. The actual amount posted to the CE obligation equals the CE minus the FLA ($500,000 – $35,000 = $465,000).

After the MC closes, there is a material hit to the local economy when a local whoopee pie company closes, devastating tourism in the area, and one of the borrowers (of a loan sold into the MC) is unable to make mortgage loan payments, and the property is foreclosed upon. There is no equity in the home, nor does the loan have PMI, and as a result, there is a loss that totals $120,000.

The impact:

Since there is no equity or mortgage insurance to cover the loss on the loan, the loss will first be absorbed by the third tranche, the FLA posted by FHLBank Boston. The value of this FLA account was $35,000, which is insufficient to cover the full loss. The remaining balance of the loss of $85,000 ($120,000-$35,000 = $85,000) will be absorbed by the CE obligation. The CE obligation began at a balance of $465,000 and will now be reduced to $380,000. Additionally, future performance-based CE income will be recouped by FHLBank Boston from Wicked Good to offset the loss to the FLA.

| Borrower Equity | Negative, no equity available |

|---|---|

| PMI | No PMI available |

| First Loss Account | $35k available to absorb losses and is fully utilized |

| PFI CE Obligation | Remaining $85k of losses absorbed, $380k remains |

Case Study Three: Catastrophic Credit Loss Occurs, Impacting both FHLBank Boston and the PFI

A PFI in Connecticut called “Nutmeg Numbers Bank” sold $10,000,000 mortgage loans to FHLBank Boston. The CE obligation was 5%, or $500,000. The FLA posted by FHLBank Boston is 35 basis points of the unpaid principal balance of the sold loans, or $35,000. The actual amount posted to the CE obligation equals the CE minus the FLA ($500,000 – $35,000 = $465,000).

After the MC closes, a massive housing crisis in Connecticut follows a mozzarella shortage, which impairs Connecticut’s well-recognized ability to produce the best pizza in the country. The owner of a pizza shop is unable to make his loan payments. There is no equity in the home, nor does the loan have PMI, and, as a result, there is a loss that totals $600,000.

The impact:

There is no equity or mortgage insurance to cover the loss on the loans, so the loss will first be absorbed by the third tranche, the FLA posted by FHLBank Boston. The value of this FLA account was $35,000, which is insufficient to cover the full loss. After this tranche, the remaining loss balance is $565,000 ($600,000 – $35,000 = $565,000). The next tranche, the CE obligation, has a value of $465,000. This tranche is also inadequate to cover the losses associated with these mortgage loans and will be depleted entirely. Even after this tranche is depleted, the remaining loss balance is $100,000 ($565,000 – $465,000 = $100,000). This last $100,000 will be absorbed by FHLBank Boston.

| Borrower Equity | Negative, no equity available |

|---|---|

| PMI | No PMI available |

| First Loss Account | $35k available to absorb losses and is fully utilized |

| PFI CE Obligation | $465k available to absorb losses and is fully utilized |

| FHLBank Boston | Remaining $100k of losses absorbed here |

Additional MPF Products

Please note that this document summarizes key points of the MPF Traditional Program, but FHLBank Boston also offers modified versions of the Traditional Program to support housing finance. These include the Permanent Rate Buydown, which is designed to support borrowers with incomes up to 80% of the area’s median income, and MPF Xtra®, which focuses on mortgage loans eligible for sale to Fannie Mae and has no credit risk-sharing component.

Conclusion

MPF supports FHLBank Boston’s housing financing mission by empowering PFIs to focus on credit risks in their local communities. MPF allows participating members to better access liquidity, reduce interest-rate risk, and moderate credit risk. It provides an alternative or supplemental option to other secondary market sales outlets. If you’re interested in learning more about MPF and how you can participate, please reach out to our Member Services team.

“Mortgage Partnership Finance” and “MPF” are registered trademarks of the Federal Home Loan Bank of Chicago.

FHLBank Boston does not act as a financial advisor, and members should independently evaluate the suitability and risks of all advances. The content of this article is provided free of charge and is intended for general informational purposes only. FHLBank Boston does not guarantee the accuracy of third-party information displayed in this article, the views expressed herein do not necessarily represent the view of FHLBank Boston or its management, and members should independently evaluate the suitability and risks of all advances.

Forward-looking statements: This article uses forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 and is based on our expectations as of the date hereof. All statements, other than statements of historical fact, are “forward-looking statements,” including any statements of the plans, strategies, and objectives for future operations; any statement of belief; and any statements of assumptions underlying any of the foregoing. The words “expects”, “may”, “likely”, “continue”, “possible”, “to be”, “will,” and similar statements and their negative forms may be used in this article to identify some, but not all, of such forward-looking statements. The Bank cautions that, by their nature, forward-looking statements involve risks and uncertainties, including, but not limited to, the uncertainty relating to the timing and extent of FOMC market actions and communications and economic conditions (including effects on, among other things, interest rates and yield curves). The Bank reserves the right to change its plans for any programs for any reason, including but not limited to legislative or regulatory changes, changes in membership, or changes at the discretion of the board of directors. Accordingly, the Bank cautions that actual results could differ materially from those expressed or implied in these forward-looking statements, and you are cautioned not to place undue reliance on such statements. The Bank does not undertake to update any forward-looking statement herein, or that may be made from time to time on behalf of the Bank.

As a senior financial strategist at FHLBank Boston, Caroline helps members navigate complex market conditions with clarity and confidence.