Short-Term Rates with Long-Term Liquidity

Andrew Paolillo

Several advance solutions exist to calibrate interest-rate risk and liquidity needs to different parts of the yield curve.

Rates Have Moved Up, More Increases Could Be on the Way

Two years after lowering interest rates to near-zero levels and embarking on a historic bond purchasing program, the Federal Reserve has begun to raise rates and is preparing to shrink the size of its balance sheet. After increasing the target Fed Funds range by 0.25% in March and then by another 0.50% in May, market expectations for further hikes remain exceptionally high. And there’s chatter about a possible 0.75% increase being on the table.

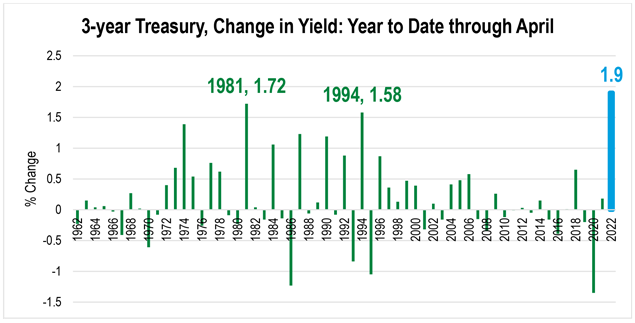

As an example of the expectation that short-term rates will continue to rise over the near term, consider the recent path of the three-year Treasury note, which experienced the largest year-to-date basis point move (through April) in the last 60 years.

In addition to this uptick in volatility which has pushed interest rates higher, instruments such as mortgage loans, mortgage-backed securities, corporate bonds, and municipal bonds have all exhibited weakness (independent of the impact of interest-rate movements) and seen their spreads widen. One notable exception is high-quality commercial real estate loans, where the persistence of depositories with high levels of excess liquidity has kept pricing in check as demand for loans remain high.

FHLBank Boston has several floating-rate advance solutions that allow balance sheet managers to mitigate the different risks they are tasked with juggling.

Liquidity conditions have also been impacted by the onset of the Fed tightening cycle. More appealing rates and spreads on asset alternatives has led to a reduction of cash on balance sheets, and we’ve observed a noticeable slowdown in deposit growth rates, and in some cases net deposit outflows, for our depository members. Current excess liquidity levels and experience from the last hiking cycle which occurred from 2015 to 2018 has led many to expect deposit betas to stay low and allow for significant pricing lags as the Fed hikes rates, specifically for the first 100 basis point of increases. But with the Fed on track to hit 100 basis points of hikes within just three months compared to the 18 months it took last time for the first 100 basis points of hikes to be realized, normalization of liquidity levels may occur faster than forecast.

Disintermediating Interest-Rate and Liquidity Risks

Often, the point on the yield curve that a financial institution seeks to add an asset or liability may not necessarily be the same when it comes to balance return with interest-rate and liquidity risks. For example, many of our depository members are asset sensitive and an optimal profile for incremental funding may be with short-term rate exposure combined with longer-term average lives on assets. Insurance companies purchasing long assets may seek to extend funding out in lockstep to obtain operational leverage treatment, but if the assets are floating rate, then the funding needs to match. FHLBank Boston has several floating-rate advance solutions that allow balance sheet managers to mitigate the different risks they are tasked with juggling. Below we will look at a few examples.

Strategy #1: Using the Discount Note Auction-Floater Advance

The Discount Note Auction-Floater Advance, or DNA Floater, can be a useful floating-rate alternative for members in three distinct ways:

- A commonly used structure for a DNA Floater is a one-year maturity with a rate that resets every four weeks. By extending the maturity, the DNA Floater is more liquidity metric-friendly than a one-month Classic Advance and has the same repricing frequency.

- The DNA Floater affords the member the option to prepay the advance with no fee at every rate reset interval. This is particularly useful for members managing uncertain deposit flows, where today’s outflows and diminished growth may reverse at some point in the future.

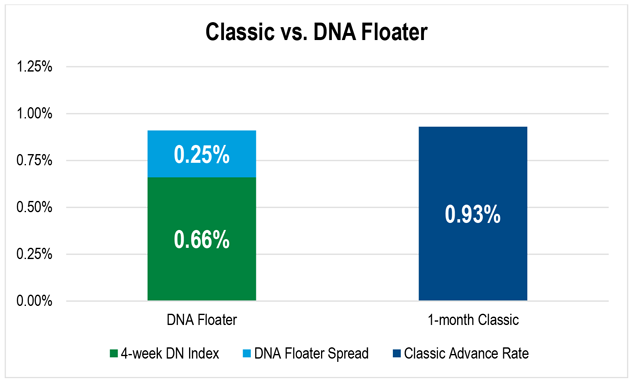

- Available at several long-term maturities, the DNA Floater may offer pricing benefits depending on market conditions. In the example below, a DNA Floater with a one-year maturity and a four-week reset was recently priced at an all-in rate of 0.91% — 0.66% for the base rate of the discount note index, and 0.25% for the advance spread. This is a savings of two basis points when compared to the Classic Advance at 0.93%, but offers the same ability/cost to collapse the advance (i.e. let the Classic Advance mature or call the DNA Floater at the first reset) yet benefit from the longer maturity and ability to retain the locked-in spread if so desired.

Strategy #2: Using the SOFR-Indexed Advance to Benefit if Hikes Underperform Expectations

While the consensus is that short-term rates will reach 2% or even 3% in relatively short order, many know from experience that markets don’t always perform as expected. The SOFR-Indexed Advance and the Callable SOFR-Indexed Floater Advance can be appealing options for those seeking to position the balance sheet to benefit if the Fed does not hike rates to the expected magnitude and timing.

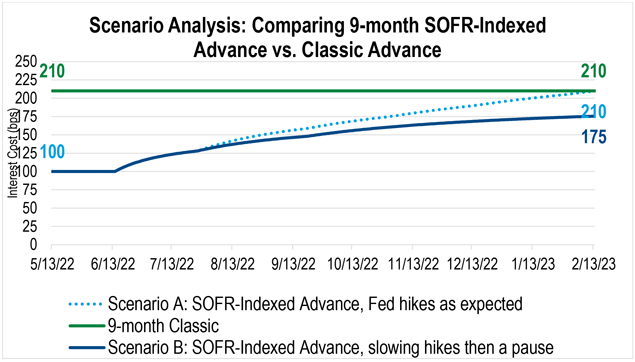

Consider the scenario analysis below, which compares the all-in rate of a nine-month SOFR-Indexed Advance at +21 and the fixed-cost of a nine-month Classic Advance at 2.10% under different Fed hiking assumptions. The floater cost will be equivalent to the fixed-rate cost if there are 0.50% hikes in June and July, followed by four consecutive 0.25% hikes (Scenario A). However, if we assume the Fed hikes rates by 0.50% in June and conditions warrant two more 0.25% hikes and then a pause, the floater will sharply outperform the fixed-rate product (Scenario B).

Strategy #3: Using a Blend of SOFR Advances and DNA Floater Advances for Spread Lending

A popular strategy for insurance companies is to use floating-rate advances to fund investment opportunities. When the asset is prepayable and/or amortizing, as is the case with collateralized loan obligations or mortgages, constructing a funding portfolio that leans on the callability of the DNA Floater and laddering Callable SOFR-Indexed Floater Advances can help strike the appropriate balance of maximizing spread income while aligning the cash flows with that of the asset.

The table below compares the total day-one interest cost, the final maturity, and the shortest average life for two strategies using the call features of the DNA Floater and Callable SOFR-Indexed Floater Advances.

The first approach uses a DNA Floater with a five-year maturity and 13-week reset as the sole funding vehicle. The second strategy uses the same DNA Floater for only 50% of the target amount, and 25% apiece in Callable SOFR-Indexed Floater Advances — a 13-month maturity with a member call option at the 12-month mark and a three-month, two-month structure. The blended approach produces a lower interest expense of 20 basis points, with a maturity of nearly three years, and a shorter average life of just under five months, which affords the flexibility to account for uncertain paydowns on the asset portfolio.

| Strategy | Day 1 Interest Cost | Final Maturity | Shortest Average Life |

|---|---|---|---|

| Blended Strategy (DNA & Callable SOFR) | 1.19% | 2.83 | 0.42 |

| DNA Only | 1.39% | 5 | 0.25 |

Flexible Funding

Recent market conditions have created challenges and opportunities for FHLBank Boston members. Our Financial Strategies group has developed a suite of analytical tools designed to help you identify the funding solutions that best fit the unique needs of your balance sheet. Please contact me at 617-292-9644 or andrew.paolillo@fhlbboston.com or reach out to your relationship manager for more details.

FHLBank Boston does not act as a financial advisor, and members should independently evaluate the suitability and risks of all advances. The content of this article is provided free of charge and is intended for general informational purposes only. FHLBank Boston does not guarantee the accuracy of third-party information displayed in this article, the views expressed herein do not necessarily represent the view of FHLBank Boston or its management, and members should independently evaluate the suitability and risks of all advances. Forward-looking statements: This article uses forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 and is based on our expectations as of the date hereof. All statements, other than statements of historical fact, are “forward-looking statements,” including any statements of the plans, strategies, and objectives for future operations; any statement of belief; and any statements of assumptions underlying any of the foregoing.. The words “expects”, “may”, “likely”, “could”, “to be”, “will,” and similar statements and their negative forms may be used in this article to identify some, but not all, of such forward-looking statements. The Bank cautions that, by their nature, forward-looking statements involve risks and uncertainties, including, but not limited to, the uncertainty relating to the timing and extent of FOMC market actions and communications; economic conditions (including effects on, among other things, interest rates and yield curves); and changes in demand and pricing for advances or consolidated obligations of the Bank or the Federal Home Loan Bank system. The Bank reserves the right to change its plans for any programs for any reason, including but not limited to legislative or regulatory changes, changes in membership, or changes at the discretion of the board of directors. Accordingly, the Bank cautions that actual results could differ materially from those expressed or implied in these forward-looking statements, and you are cautioned not to place undue reliance on such statements. The Bank does not undertake to update any forward-looking statement herein or that may be made from time to time on behalf of the Bank.

As vice president, director of member strategies and solutions at FHLBank Boston, Andrew leads the Strategy team in creating customized funding strategies for members.