Products and Solutions Guide

Introduction

Building Communities – Building New England

The mission of the Federal Home Loan Bank of Boston is to provide highly reliable wholesale funding and liquidity to its member financial institutions in New England. We deliver competitively priced financial products, services, and expertise that support housing finance, community development, and economic growth, including programs targeted to lower-income households.

Chartered in 1932, the Federal Home Loan Bank of Boston is one of 11 Federal Home Loan Banks across the country. The Bank is a cooperative that serves the six New England states. Our members are our shareholders and our customers, and we are committed to providing members with financial products and services that help build vibrant communities within established risk management parameters.

The Products and Solutions Guide1 is designed to help members understand and use our products, solutions, services, and pricing. It also provides information about the Bank’s credit and collateral policies, the Mortgage Partnership Finance® (MPF®) program, and the requirements for accessing those products and services in a safe and sound manner.

About the Guide

The Bank’s board of directors established the Products and Solutions Guide and reviews and re-adopts it at least annually. It is available here for review or by contacting the Collateral Department at 800-357-3452 or by email collateral@fhlbboston.com.

In the event of any conflict between the terms of this Products and Solutions Guide and any prior versions of the Bank’s Credit Policy or the Bank’s Products Policy, this Products and Solutions Guide shall control.

1. The Products and Solutions Guide serves as the Bank’s Products Policy in accordance with 12 CFR Part 1239.30.

Mortgage Partnership Finance®, MPF®, MPF Xtra®, eMPF®, and MPF® Direct are registered trademarks of the Federal Home Loan Bank of Chicago.

Products and Solutions Overview

Credit Products

The Bank offers short-, medium-, and long-term loans known as advances. These advances offer fixed or variable rates and several choices for payment of principal and interest.

The Bank also offers forward commitments to take down advances. Some advances contain embedded options, interest-rate caps, or interest-rate floors. The Bank offers discounted advances for funding eligible affordable-housing and community-development initiatives. In addition to advances, the Bank offers noncash credit products such as letters of credit.

We want our members to have the tools and information necessary to select the best financial solutions. In addition to your relationship manager, the Bank’s financial strategists are available to produce an analysis that can help guide you to ultimately select the funding solution that meets your specific needs. Our strategists may be reached at 800-357-3452 or via e-mail at strategies@fhlbboston.com.

Please note that the Bank does not act as a financial adviser, and members should independently evaluate the suitability and risks of our solutions. Please fully assess these risks and their implications prior to obtaining products from the Bank. We strive to make all maturities available every business day, subject to market conditions.

For more information about our credit products, please call your relationship manager or the Member Funding Desk at 800-357-3452, or consult the Products & Programs section of the Bank’s website.

The product and solution descriptions that appear in the following pages of this guide are meant as summaries only and do not purport to disclose all risks and other material terms and conditions associated with such products and solutions. Nothing in this guide shall be deemed business, legal, tax, or accounting advice from the Bank. Members are encouraged to consult their own business, legal, and accounting advisers with respect to the Bank’s products and solutions and should refrain from utilizing any of the Bank’s products and solutions unless they have fully assessed the risks and terms.

The Bank’s confirmations for advances are available in Appendix D of this guide. A member should review not only this guide, but also the advance confirmation associated with any Bank product or solution prior to utilizing such product or solution so as to understand the terms, including, without limitation, the prepayment provisions.

Overnight Funding

Daily Cash Manager Advance

Description

Overnight funding.

Common Uses

- Manage daily liquidity needs.

Terms

One day.

Disbursement

Funds are available the same day or next business day.

Principal and Interest

- Principal and interest are due at maturity, which is the next business day.

- Interest is calculated on an actual/360-day basis.

Rollover Cash Manager Advance

Description

Overnight funding with an automatic rollover at maturity.

Common Uses

- Manage daily liquidity needs.

Terms

Maturity is one day, with an automatic rollover to a new one-day advance at the prevailing rate.

Disbursement

Funds are available the same day or next.

Principal and Interest

- Principal may be paid on a date you choose.

- Payment of interest is due monthly on the second business day of the month.

- Interest is calculated on an actual/360-day basis.

IDEAL Cash Manager Advance

Description

Overnight funding using your IDEAL Way Line of Credit.

Common Uses

- Manage daily liquidity needs.

Terms

One day.

Disbursement

Funds are available the same day and can be accessed by wiring funds from your IDEAL Way demand account, causing an overdraft.

Principal and Interest

- Principal is due at maturity. Payment of interest is due monthly on the second business day of the month.

- Interest is calculated on an actual/360-day basis.

Additional Information

- Capital stock deficiencies caused by IDEAL Cash Manager advances will be automatically satisfied through a capital stock purchase prior to the payoff of the advance.

The IDEAL Way Line of Credit

- The IDEAL Way Line of Credit allows members to access liquidity quickly and conveniently, without calling the Member Funding Desk.

- It is a fixed amount, typically 2% of assets, and can easily be set up and/or changed by the member by making a request through the Member Funding Desk.

- Members are required to maintain collateral equal to the entire amount of the IDEAL Way Line of Credit, whether used or not.

- For more information about the IDEAL Way Line of Credit, please contact the Member Funding Desk at 800-357-3452 or memberfunding@fhlbboston.com.

Fixed-Rate Advances

AHP Subsidized Amortizing Advance

Description

A fixed-term and rate advance with an amortizing principal using Affordable Housing Program subsidy funds to reduce the interest rate for the member.

Common Uses

- Fund long-term affordable housing assets whose principal balance declines on a monthly basis due to amortization and/or prepayment.

AHP Overview

The Federal Home Loan Bank of Boston’s Affordable Housing Program, in partnership with member institutions, supports affordable housing needs across New England and elsewhere. A portion of the Bank’s net earnings funds the program, which awards grants and low-interest advances (loans) through member institutions.

The AHP encourages local planning of affordable-housing initiatives. The Bank’s member institutions work with housing organizations to apply for funds to support initiatives that serve very low- to moderate-income households in their communities.

Funding for projects submitted to the AHP by member institutions is awarded annually in at least one competitive round. Subsidized advances (loans) and direct subsidies (grants) are available. Terms are determined by the member applicant based on the needs of the development. Approval of funding or interest-rate subsidies is made through a competitive application process and is not guaranteed.

Terms

Maturities available for terms of 10 years out to 20 years with principal-amortization periods out to 30 years.

Disbursement

Bank review of requests for approved AHP subsidized advances is required prior to disbursement. Once reviewed, funds will be available the same day if requested by noon and the following day if requested by 3:00 p.m.

Principal and Interest

- Principal and interest are due on the first business day of the month.

- Interest is calculated on an actual/360-day basis.

Prepayment

Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which includes additional information on prepayment fees.

Amortizing Advance

Description

A fixed-term and rate advance with an amortizing principal.

Common Uses

- Fund short- or long-term assets whose principal balance declines on a monthly basis due to amortization and/or prepayment.

Terms

Maturities available for terms out to 20 years with principal-amortization periods out to 30 years.

Disbursement

Funds will be available the same day if you call by noon and the following day if requested by 3:00 p.m.

Principal and Interest

- Principal and interest are due on the first business day of the month.

- Interest is calculated on an actual/360-day basis.

Prepayment

Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which includes additional information on prepayment fees.

CDFI Advance

Description

Members can fund enterprise-level lending to non-depository certified Community Development Financial Institutions (CDFIs) throughout New England using this 0% interest-rate advance. CDFI Advances must be used by the recipient CDFI to support the development of affordable housing, job creation/small business growth, or the expansion of community facilities in distressed communities throughout New England. CDFIs must use the funding in accordance with an eligible activity in their target market as defined by the Community Development Financial Institutions Fund.

Common Uses

- Members loan funds to the certified CDFI at the enterprise level.

- The CDFI must use program funds to provide direct lending or investment in the form of:

- affordable home mortgages,

- affordable housing development loans or investments,

- home improvement loans,

- small business loans or investments or

- commercial real estate development loans or investments to residents or businesses that meet one or more Target Market components.

Approval

Preapproval is necessary through an application on the Bank’s Community Lending portal. Annual approvals are limited up to the maximum advance amount per member and per CDFI, as set for the funding round.

Term and Rate

Available as a Classic Advance for a term of five years. The interest rate on CDFI Advances is set to 0%. Members may add up to 300 basis points as a spread when lending to the CDFI.

Disbursement

Bank review is required prior to disbursement. Once reviewed, funds are typically available the same day if you call by noon and the following day if you call by 3:00 p.m.

Principal and Interest

- Principal is due at maturity, and interest is due on the second business day of the month.

- Interest is calculated on an actual/360-day basis.

Prepayment

Please see the CDFI Advance Confirmation for more information.

Reporting

The Bank requires members to supply two reports. First, the member must confirm passthrough of all program funds to an eligible CDFI. Second, within 180 days of disbursement, the recipient CDFIs must supply a listing of all end-borrower loans made with CDFI Advances funding to the member. The member must provide this listing to the Bank. As part of this submission, the member must complete a short, one-time online report describing how the funds were used.

Classic Advance

Description

Nonamortizing, fixed-term and rate advance.

Common Uses

- Manage liquidity needs.

- Manage interest-rate risk.

- Fund short- or long-term assets.

Terms

Maturities available for terms out to 30 years.

Disbursement

Funds are typically available the same day if you call by noon. They are available the following day if requested by 3:00 p.m.

Principal and Interest

- Principal is due at maturity, and interest is due on the second business day of the month.

- For advances with maturities of one year or less, you may choose to pay principal and interest at maturity. If chosen, the advance rate may be higher than the posted rate.

- For advances with maturities of more than one year, principal is due at maturity, and interest is due either monthly, on the second business day of the month, or semiannually. If interest is due semi-annually, the advance rate may be higher than the posted rate.

- Interest is calculated on an actual/360-day basis.

Prepayment

Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which has additional information on prepayment fees.

Community Development Advances

Description

Discounted advances that support affordable housing and economic development initiatives.

Annual approvals per member are limited to:

- $100 million for CDA;

- and $50 million for CDA Extra.

Types

CDA

Discounted advance that supports a variety of economic development and mixed-use initiatives, including loans for small businesses, social-service or public-facility initiatives, and infrastructure improvements. These advances can also be used to support commercial, industrial, and manufacturing initiatives:

- Initiatives benefitting households with incomes at or below 115% of area median income for a rural initiative, or 100% of AMI for an urban initiative for a family of four, based on the income guidelines as published annually by HUD.

- Initiatives located in a census tract at or below 115% of AMI for a rural initiative or 100% of AMI for an urban initiative.

CDA Extra

Deeply discounted advance that supports:

- Affordable housing initiatives serving households at or below 115% of AMI.

- Economic development or mixed-use initiatives serving households at or below 80% of AMI.

Terms

Pre-approval is necessary. To apply for a Community Development advance, members must submit an online application.

Disbursement

Members must take down a Community Development advance within six months of the date of approval, unless the application included an approved request for a longer take-down period. Funds are typically available the same day if you call by noon, and the following day if you call by 3:00 p.m.

Principal and Interest

- Based on product type (see page for specific product).

Available Products and Maturities

Not all advance structures are available as CDA. Please contact the Member Funding Desk or your relationship manager for available products and maturities.

Reporting

The Bank requires reporting for Community Development advances at the time of application or at disbursement.

Prepayment

Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which has additional information on prepayment fees.

Forward Starting Advance

Description

Lock in current fixed rates and delay funding the advance for up to two years. Classic and Amortizing advances may be customized to use the forward starting feature.

Common Uses

- Access the current rate environment without adding additional liquidity.

- Lock in rates for anticipated future funding needs.

- Allow borrowers to lock in rates on loans with future closing dates.

- Manage anticipated deposit runoff or uncertainty in the future.

Terms

Maturities available for terms out to 20 years.

Disbursement

Funding can be delayed for up to two years.

Principal and Interest

- Principal and interest are due based on the terms of the specific advance utilized. Interest begins accruing at disbursement.

- Interest is calculated on an actual/360-day basis.

Additional Information

- Members will be required to collateralize and purchase activity-based capital stock at the time of disbursement.

- Please call the Member Funding Desk at 800-357-3452 for indications on specific structures.

HLB-Option Advance

Description

Nonamortizing, fixed-rate and term advance. The Bank holds the option to cancel the advance on specified dates prior to maturity.

Common Uses

- Generally used in a flat yield-curve environment to obtain a lower cost of funding than a Classic Advance with a maturity equal to the lockout period.

- Fund short- or long-term assets.

Terms

- Maturities available for terms out to 20 years, but always with the condition that the Bank may cancel the advance prior to final maturity.

- There is an initial lockout period during which the Bank cannot cancel the advance. You may choose a lockout period of three months to 10 years.

- We may cancel the advance only on scheduled cancellation dates, after the initial lockout period. The Bank makes no warranties as to the circumstances under which it might cancel an advance.

- The Bank will provide written notice of cancellation at least four business days before the cancellation date.

- Some HLB-Option Advances are offered with only one cancellation date. Others are offered with a series of cancellation dates at regular intervals, usually quarterly.

- The minimum offering size is $2 million. Offering size orders for less than $2 million will be aggregated with other requests for advances with identical terms and will be executed when orders total $2 million.

Disbursement

Funds are available two business days after the trade date.

Principal and Interest

- Principal is due at maturity, and interest is due on the second business day of the month.

- If the Bank exercises its option to cancel, you must repay the advance, but you may replace the advance with a new advance. The new advance may be for any structure and term to maturity agreed upon between the member and the Bank. The rate on the new advance will be that in effect at the time the new advance is taken.

- Interest is calculated on an actual/360-day basis.

Prepayment

Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which has additional information on prepayment fees.

Jobs for New England Advance

Description

Members can access 0% advances for small-business loans and other eligible economic development lending. Jobs for New England is designed to support small businesses as defined under the SBA 504 program, as well as women, minority, and veteran-owned businesses. A key objective is the creation or preservation of jobs in New England.

Common Uses

- Supports communities served by members.

- Assists local businesses with capital improvements, equipment purchases, and ownership changes.

- Combines with other funding to meet business needs.

- Potential for Community Reinvestment Act credit.

Approval

Preapproval is necessary through an application on the Bank’s Community Lending portal. Annual approvals are limited up to the interest-rate subsidy maximum per member, as set for the funding round.

Terms

Available as Classic Advance in terms from one to 10 years.

Disbursement

Bank review is required prior to disbursement. Once reviewed, funds are typically available the same day if you call by noon and the following day if you call by 3:00 p.m.

Principal and Interest

- Principal is due at maturity, and interest is due on the second business day of the month.

- Interest is calculated on an actual/360-day basis.

Prepayment

Please see the Jobs for New England Confirmation for more information.

Reporting

The Bank requires reporting within one month of the disbursement of the advance.

Member-Option Advance

Description

Nonamortizing, fixed-term and rate advance. Members have the option to cancel the advance on specified cancellation dates they select.

Common Uses

- Manage interest-rate risk.

- Fund short- or long-term assets.

- Manage exposure to prepayment risk of assets.

Terms

- Maturities are available for terms out to 20 years.

- The member must provide written notice of cancellation at least four business days before the cancellation date.

- The minimum offering size is $2 million. Offering size orders for less than $2 million will be aggregated with other requests for advances with identical terms and will be executed when orders total $2 million.

Disbursement

Funds will be available three business days after the trade date.

Principal and Interest

- Payment of principal is due at maturity. Interest is due monthly on the second business day of the month.

- Interest is calculated on an actual/360-day basis.

Prepayment

- Advances may be prepaid in full or in part, on specified cancellation dates with no prepayment fee. Typically, the cancellation dates are the first or third anniversary of the disbursement and semiannually thereafter. (Other prepayment structures may be available.)

- The advance may be prepaid, subject to a fee, on any date other than a specified cancellation date.

Please see the Member-Option Advance Confirmation for more information on prepayment fees.

New England Fund

Description

Discounted advances that support affordable housing initiatives.

The New England Fund (NEF) offers low-cost, fixed-rate advances to support eligible affordable housing initiatives that benefit households with incomes at or below 80% of the area median family income.

Member institutions may apply to the NEF for funding in support of proposed developments, programs, or loans that meet the eligibility guidelines specified below.

Income Guidelines

Where mentioned below, “area median income” and AMI refer to the area median income as defined by the U.S. Department of Housing and Urban Development. You can use the Federal Financial Institutions Examination Council’s Geocoding System to determine the median-income percentage for a particular address.

Ownership Initiative

- An ownership initiative is eligible if it is: Part of a Massachusetts 40B initiative where the loan supports an “affordable” subdivision or condominium where the incomes of at least 25% of the individual homeowners will not exceed 80% of the AMI;

- Part of a Massachusetts 40R initiative where at least 20% of the units are targeted for households earning 50% or below of the area median income; or

- Part of a Massachusetts 40R initiative or Rhode Island Comprehensive Permit initiative, where the loan supports an “affordable” subdivision or condominium where the incomes of at least 20% of the individual homeowners will not exceed 80% of the AMI.

Rental Initiative

A multifamily rental or cooperative initiative is eligible if it is:

- Part of a Massachusetts 40B initiative where 25% of the units are affordable to residents whose incomes do not exceed 80% of the AMI;

- Part of a Massachusetts 40R initiative where at least 20% of the units are targeted for households earning 50% or below of the area median income; or

- Part of a Massachusetts 40R initiative or Rhode Island Comprehensive Permit initiative, where at least 20% of the units are affordable to residents whose incomes do not exceed 80% of the AMI.

Terms

Pre-approval is necessary. To apply for the NEF advance, members must submit an online application.

Disbursement

Members must take down an NEF advance within 12 months of the approval date, unless the application included an approved request for a longer take-down period.

Available Products and Maturities

NEF advances are available with maturities out to 20 years. Classic, Member-Option, and Amortizing advances are available as NEF advances.

Reporting

The Bank does not require annual reporting for NEF advances, but it does reserve the right to monitor compliance with the certifications made in the confirmation for the advance.

Prepayment

Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which has additional information on prepayment fees.

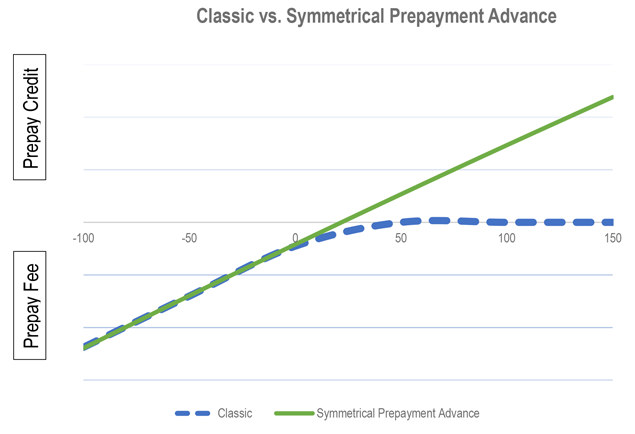

Symmetrical Prepayment Advance

Description

Nonamortizing, fixed-term and rate advance with a special prepayment feature that allows you to prepay the advance at its approximate market value. Any gain will be passed through to the member subject to certain limitations.

Common Uses

- Manage liquidity needs.

- Manage interest-rate risk.

- Fund short- or long-term assets.

- In a rising-rate environment, the gain from prepayment can be used to offset the loss on sale of securities or other assets.

Terms

- Maturities are available for terms out to 20 years.

- The minimum offering size is $2 million. Offering size orders for less than $2 million will be aggregated with other requests for advances with identical terms and will be executed when orders total $2 million.

Disbursement

Funds are available next day.

Principal and Interest

- Payment of principal is due at maturity, and interest is due on the second business day of the month.

- Members may choose monthly or semiannual interest payments prior to initiation.

- Interest is calculated on an actual/360-day basis.

Prepayment

- For further detail, please see the Comparison of Prepayment Profile below.

- Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which has additional information on prepayment fees.

Comparison of Prepayment Profile

Long-Term Variable-Rate Indexed Advances

Callable SOFR-Indexed Floater Advance

Description

Nonamortizing, fixed-term advance with an interest rate that adjusts daily, according to changes in SOFR. Members have the option to cancel the advance on specified cancellation dates they select.

Common Uses

- Manage liquidity needs.

- Fund adjustable-rate assets.

- Manage exposure to declining interest rates.

- Long-term funding commitments at short-term interest rates.

- Manage prepayment risks.

- Reduce funding costs.

Terms

- Maturities are available out to 20 years.

- The minimum offering size is $2 million. Offering size orders for less than $2 million will be aggregated with other requests for advances with identical terms and will be executed when orders total $2 million.

Disbursement

Funds are available two business days after the trade date.

Principal and Interest

- Principal is due at maturity. Interest is due quarterly, the following business day after the anniversary date of settlement.

- During the lockout period, rates adjust daily, based on SOFR.

- Rate adjusts daily; Subject to an index floor of 0%.

- Interest is calculated on an actual/360-day basis.

Prepayment

- Advances may be prepaid in full or in part, on specified cancellation dates with no prepayment fee. Notice of cancellation must be received no fewer than nine business day prior to a specified cancellation date.

- Advances may be prepaid, subject to a fee, on any date other than a specified cancellation date. Please see Appendix D to find the confirmation statement, which has additional information on prepayment fees.

Discount Note Auction-Floater Advance

Description

Nonamortizing, fixed-term advance with an interest rate that adjusts periodically according to changes in the Federal Home Loan Bank System’s Office of Finance discount note auction rates.

Common Uses

- Manage liquidity needs.

- Fund adjustable-rate assets.

- Manage exposure to declining interest rates.

- Long-term funding commitment at short-term interest rates.

Terms

- Maturities are available in terms out to 20 years.

- The minimum offering size is $2 million. Offering size orders for less than $2 million will be aggregated with other requests for advances with identical terms and will be executed when orders total $2 million.

Disbursement

Funds are available the next day.

Principal and Interest

- Principal is due at maturity. Interest is due on the rate-adjustment date.

- Rates reset every four or 13 weeks, depending on the index you choose, on indicated reset dates, based on the result of the prior day’s discount-note auction.

- Interest is calculated on an actual/360-day basis.

Prepayment

Advances may be prepaid, subject to a fee. There is no fee if paid at reset dates. Please see the Discount Note Auction-Floater Advance Confirmation for more information on prepayment fees.

SOFR Flipper Advance

Description

Nonamortizing, floating-to-fixed-rate advance where the Bank holds the option to cancel the advance on certain specified dates after a specified lockout period. During the lockout period, the advance rate will adjust daily according to changes in SOFR and may be sub-SOFR (the spread to SOFR is determined by the member). If the advance is still outstanding after the lockout period, it will flip to a predetermined fixed rate.

Common Uses

- Generally used in a flat yield curve environment when margins are under pressure

- Match fund adjustable assets

- Protects against falling rates

- Manage interest-rate risk

- Reduces funding costs

Terms

- Maturities are available out to 20 years. FHLBank Boston may cancel the advance prior to final maturity.

- You may choose a lockout period of three months to 10 years. We may cancel the advance at the end of the lockout period on a scheduled cancellation date, but not prior. A notice will be provided in writing at least four business days before the cancellation date.

- The Bank makes no warranties as to the circumstances under which we might cancel an advance.

- Certain SOFR Flipper Advances are offered with only one cancellation date. Others are available with a series of cancellation dates at regular quarterly or annual intervals.

- The interest rate can reset at a rate less than zero.

- The Bank holds the option to cancel on certain specified dates. If the advance is not cancelled at the end of the lockout period, the advance will convert, or flip, into a fixed-rate advance. We may cancel the advance on any subsequent scheduled cancellation date, if any.

- The minimum offering size is $2 million. Offering size orders for less than $2 million will be aggregated with other requests for advances with identical terms and will be executed when orders total $2 million.

Disbursement

Funds are available two business days after trade date.

Principal and Interest

- Principal is due at maturity. Interest is due quarterly, from disbursement date.

- During the lockout period, rates adjust daily, based on SOFR.

- If the Bank exercises its option to cancel, you must repay the advance, but you may replace it with a new advance. The new advance may be for any structure and term to maturity agreed upon between you and the Bank. The rate on the new advance will be that in effect at the time the new advance is taken.

- Interest is calculated on an actual/360-day basis.

Prepayment

Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which has additional information on prepayment fees.

SOFR-Indexed Advance

Description

Nonamortizing, fixed-term advance with an interest rate that adjusts daily, according to changes in SOFR.

Common Uses

- Manage liquidity needs.

- Fund adjustable-rate assets.

- Manage exposure to declining interest rates.

- Long-term funding commitments at short-term interest rates.

Terms

- Maturities are available out to 20 years.

- The minimum offering size is $2 million. Offering size orders for less than $2 million will be aggregated with other requests for advances with identical terms and will be executed when orders total $2 million.

Disbursement

Funds are available two business days after trade date.

Principal and Interest

- Principal is due at maturity. Interest is due annually, two business days after the anniversary date of settlement.

- Rate adjusts daily.

- Interest is calculated on an actual/360-day basis.

Prepayment

Advances may be prepaid, subject to a fee. Please see Appendix D to find the confirmation statement, which has additional information on prepayment fees.

Advance Restructuring

A solution that extends the maturity and reduces the rate of existing advances.

Through this product, members can restructure outstanding advances for certain eligible product types and blend the contractual prepayment fee into the rate of a new long-term advance. There is no cash settlement of the prepayment fee since it is blended into the rate of the new advance. This allows members to extend the maturity of their existing advances at a lower rate on the new advances compared with the rate on the original advances — without taking additional cash or purchasing additional stock.

The Bank will also remodify advances that were restructured more than 12 months ago.

To help you determine whether this product may be beneficial to your institution, please contact your relationship manager.

Advances Pricing

The Bank prices credit products consistently and without discrimination to all members applying for advances, no matter the size of the financial institution. We must also ensure regulatory compliance while making advances profitable in order to meet our financial performance objectives and provide an adequate return to our member shareholders. We strive to provide a rate that is competitive with comparable funding alternatives available to members.

We are also prohibited by regulation from pricing our advances below our marginal cost of matching term and maturity funds in the marketplace, including embedded options, and the administrative cost associated with making such advances to members. However, we may price advances on a differential basis, such as the creditworthiness of members, volume, or other reasonable criteria applied consistently to all members.

With these regulatory parameters in mind, we price all credit products according to market conditions and the following specific criteria:

- The Bank’s cost of funds;

- The Bank’s cost of delivering products (general and administrative expenses); and

- Bank profitability targets and risk/return objectives.

The Bank’s Asset-Liability Committee establishes minimum spread requirements relative to its funding costs for all products.

Please note that pricing for the Daily Cash Manager advance is primarily based on the federal funds market, which is highly variable and dynamic. As a result, pricing is subject to change more frequently and at irregular intervals compared with other advances products.

Special Advance Offerings

From time to time, the Bank offers scheduled and unscheduled specials on pricing. In order to promote equal access to “special” pricing to all members, we offer specials that approximate those offered for single large transactions.

Current and historical advance rates are available only to members on our website. Members are required to provide their work email address and enter a code sent by FHLBank Boston to that email address to access advance rates.

Please note that members also have access to advance rates through Online Banking and the Advance Rates API Service. Members with questions regarding accessing advance rates on our website or through other channels, please contact us at help@fhlbboston.com.

Letters of Credit

Description

Standby and confirming.

Common Uses

- Securing public unit deposits.

- Credit support for certain tax-exempt and taxable bonds.

- Performance guaranty in lieu of a construction performance bond.

- Collateral for obligations arising pursuant to an interest-rate swap.

- Credit support for other financial obligations.

Terms

- Terms typically available up to 10 years. Terms greater than 10 years may be available on an exception basis.

- For non-Confirming Stand-by Letters of Credit, the beneficiary must be a customer, vendor, or financial counterparty of the member.

Must be used to

- Facilitate residential housing finance or community lending.

- Assist with asset/liability management.

- Provide liquidity or other funding.

Issuance

For securing public-unit deposits, the next business day if the application is received by noon. Issuances for other uses vary, depending on complexity.

Letters of Credit Pricing and Fees

Legal fees and operational expenses incurred on a letter of credit may be passed through to the member as a processing fee.

LOC fees are calculated and billed on an actual/360 basis.

See the letter of credit pricing schedule in the Letters of Credit section of our website.

Fees upon draws on a letter of credit made by a beneficiary take into account all direct and indirect costs in satisfying the draw. Fees reflect the imputed rate of return that would have been earned and the taxes that would have been paid if the Bank were a private corporation. They are calculated by applying a cost-of-capital adjustment factor to the assets used in satisfying the draw.

Fixed Balance Letter of Credit fees are based on the face value of the letter of credit and are the greater of (a) a minimum dollar fee or (b) a fee based on the face value of the letter of credit multiplied by a basis points amount per annum determined by the maturity of the letter of credit. In the case of a confirming letter of credit supporting a bond transaction, a one-time processing fee will be added to the fee described previously under (b), and a minimum dollar fee will not apply.

Refundable Balance Letter of Credit fees are calculated in the same manner as Fixed Balance Letter of Credit fees. However, if during the term of the letter of credit the average daily balance in the account throughout the term of the LOC is below the original face amount of the Refundable Balance LOC, a portion of the fee is eligible for a refund to the member when the LOC matures (or annually, whichever occurs first).

Variable Balance Letter of Credit fees are based on the quarterly average outstanding balance of deposits that are collateralized by the letter of credit and reported to the Bank by the member, multiplied by a basis points amount per annum determined by the maturity of the letter of credit, plus a processing fee. Deposit balances must be reported within five business days of (a) the expiration date of the Variable Balance LOC, and (b) the close of each calendar quarter (provided that the Variable Balance LOC remains in effect as of the close of the calendar quarter). Average deposit balances that exceed the face value of the letter of credit are not guaranteed by the letter of credit.

Master Variable Letter of Credit fees are based on the quarterly average outstanding balance of deposits across all accounts that are collateralized by the letter of credit and reported to the Bank by the member, multiplied by a basis points amount per annum determined by the maturity of the letter of credit. Deposit balances must be reported within five business days of (a) the expiration date of the Master Variable LOC, and (b) the close of each calendar quarter (provided that the Master Variable LOC remains in effect as of the close of such calendar quarter). Average deposit balances that exceed the face value of the letter of credit are not guaranteed by the letter of credit.

Members should contact their relationship manager or the Member Funding Desk at 800-357-3452 or email memberfunding@fhlbboston.com for information regarding collateral requirements and pricing for letters of credit.

Asset-Purchase Programs

The Bank participates in the Mortgage Partnership Finance (MPF®) program, which is an attractive alternative to the traditional secondary market. Through MPF, the Bank purchases eligible mortgages from participating members. Members originate, retain or release the servicing of the loans, and are paid fees in return for maintaining a portion of the credit risk associated with the loans. The Bank manages the interest-rate, liquidity, and prepayment risks, as well as a portion of the credit risk of the loans purchased.

We also facilitate the sale of loans to Fannie Mae by participating members through the MPF Xtra® program.

The MPF program is administered by the Federal Home Loan Bank of Chicago. As the MPF Provider, FHLBank Chicago sets base prices, rates, and fees associated with various MPF products using observable third-party pricing sources as inputs to its proprietary pricing model. The Bank has the ability to adjust prices based on various criteria, including volume, credit risk, or level of interest rates. The MPF Provider publishes updated quotations on its secure eMPF® website during normal business hours. Participating members can execute delivery commitments of less than $1 million directly via the website. Larger commitments require a phone call to the MPF hotline, 877-463-6673. This practice ensures the accuracy of the price quote.

We do not adjust pricing based on the size of the delivery commitment or other factors.

For more information about our asset purchase programs, please contact the MPF team at 800-357-3452.

Mortgage Partnership Finance®, MPF®, MPF Xtra®, and eMPF®, are registered trademarks of the Federal Home Loan Bank of Chicago.

Correspondent Services

We provide a variety of correspondent services to support your cash management and investment activities. Services include IDEAL Way demand deposit accounts, IDEAL Way lines of credit, custodial mortgage accounts, funds transfer, Federal Reserve Bank account settlement, overnight investment, and securities safekeeping.

For more information about the Bank’s correspondent services, please contact your relationship manager or customer service at 800-357-3452, option 3.

Underwriting Requirements

General Requirements

The Bank’s decision to extend credit to a member is based principally on our analysis of the member’s financial condition and outlook, and while we will not extend credit beyond the borrowing capacity afforded by pledged (and discounted) collateral, we may limit lending below such borrowing capacity regardless of the level, value, and quality of the collateral. We encourage members to maintain access to a variety of sources of contingent liquidity and to test those sources periodically. For those members that wish to establish or augment their borrowing capacity with Federal Reserve Banks, the Bank may subordinate a portion of the Bank’s interest in collateral upon request by a member. Please contact your relationship manager or the Bank’s collateral department to discuss potential collateral subordination agreements and the movement of collateral currently held at the Bank if necessary.

To protect our cooperative and your investment, the Bank monitors each member’s financial condition on a continuous basis to ensure that extensions of credit are made in a safe and sound manner. Our primary tools for monitoring include quarterly financial reports, federal and state examination reports, audited financial reports, publicly available reports, and interviews with senior management during periodic financial reviews by the Credit Department. As part of this review, some members may be required to submit supplemental information prior to or when requesting an extension of credit from the Bank. Your relationship manager will notify you if this requirement applies to your institution.

The Bank also considers the financial condition of a member’s parent holding company and/or affiliates when extending credit to a member.

The Bank reserves the right not to extend credit to any member that the Bank determines, in its sole discretion, fails to meet the Bank’s underwriting guidelines.

Credit Categories

The Bank assigns each member to one of the following four credit categories based on our assessment of the member’s overall financial condition:

- Credit Category 1: Members that are in generally satisfactory financial condition.

- Credit Category 2: Members that show financial weakness or weakening financial trends in key financial indices and/or regulatory findings.

- Credit Category 3: Members with financial weaknesses that present the Bank with an elevated level of concern.

- Credit Category 4: Members with significant financial weaknesses and a high likelihood of failure over the next 12 months.

Note:

- All changes to a member’s credit category and/or borrowing status are reviewed and approved by the Bank’s Credit Committee. The Bank will notify the member of any such changes in writing.

- The collateral recordkeeping requirements vary based on the assigned credit category for depository institution members only. Please refer to the Collateral section of this guide for more information.

Limitations on Extensions of Credit and Credit Terms

A member’s total extensions of credit are generally limited, with potential exceptions, to 40% of its total assets, except that members with total assets of $50 billion or greater are generally limited to 30%. For members in a credit category of 2 or higher, the Bank will generally further reduce these limits and the maximum credit term, as noted below. Members must immediately contact the Bank’s Credit Department at 800-357-3452 if these limits are exceeded. These limits may be higher or lower depending on individual circumstances. In addition, members may not hold FHLBank Boston-exercisable put option advances (defined as HLB-Option, HLB-Option Floater [Flipper], HLB-Option Plus Cap, and the Knockout Advances (collectively, the “Option Advances”)) in an amount that exceeds 20% of the member’s assets. The Bank may grant exceptions to these limitations on a case-by-case basis.

| Credit Category | Maximum Exposure as a Percentage of Member Assets <$50 Billion | Maximum Exposure as a Percentage of Member Assets ≥$50 Billion | Maximum Term of Credit |

|---|---|---|---|

| 1 | 40% | 30% | 30 years |

| 2 | 30% | 20% | 15 years |

| 3 | 15% | 10% | 1 year |

| 4 | 5% | 5% | 1 monthest |

- The collateral recordkeeping requirements vary based on the assigned credit category for depository institution members only. Please refer to the Collateral section of this guide for more information.

Member Requests for Extensions of Credit

Members may request an extension of credit from the Bank by calling the Member Funding Desk at 800-357-3452. Many borrowing requests may also be completed through the Bank’s online banking system.

Residential Asset Form for Insurance Companies

The Bank is required to confirm that members maintain adequate residential housing finance assets, including mortgage-backed securities, equal to or greater than advances disbursed with more than a five-year term. If you will be borrowing at a term of more than five years, our Member Funding staff will ask you to complete and submit a new Residential Housing Finance Assets form found in the Forms + Applications section before borrowing. This form will ask for the total amount of housing assets from your last quarterly report. Keep in mind that the form is not required for borrowings with a term of five years or less.

Statutory Restrictions

Federal Housing Finance Agency regulations restrict the Bank’s ability to extend new credit to a member that becomes insolvent on a tangible equity capital basis unless the member’s primary regulator has requested in writing that the Bank make such advances. The Bank, in its sole discretion, may renew maturing advances to such a member for successive terms of up to 30 days each; provided, however, that the Bank will honor any written request of the member’s primary regulator that the Bank not renew such advances. The Bank may renew maturing advances to such a member for a term greater than 30 days with the written request of the member’s primary regulator. An insolvent member also may not maintain an IDEAL Way line of credit with the Bank.

Material Adverse Event

Each member is required to immediately call the Credit Department at 800-357-3452 to notify the Bank of any material adverse event and then to follow up in writing detailing the event. A “material adverse event” is one or more of the following:

- The occurrence of any event or series of events with the cumulative effect of adversely impacting the business, operations, properties, assets, or condition (financial or otherwise) of such member or any of its affiliates or its parent;

- The impairment of such member’s ability to perform its obligations under its advances agreement or other agreements with the Bank; and

- The impairment of the Bank’s ability to enforce its rights under the advances agreement or other agreements with such a member.

Additional Information

For additional information on the Bank’s underwriting requirements, please contact your relationship manager or the Credit Department at 800-357-3452.

Collateral Requirements

Description

Each member is required to pledge sufficient eligible collateral to secure advances (both new and outstanding), lines of credit, letters of credit, and other amounts payable to the Bank, and to participate in the asset purchase program.

In the true spirit of our cooperative, the Bank’s robust collateral requirements are in place to protect our members’ investments in the Bank. Every member is required to pledge the required amount of eligible collateral to secure all extensions of credit from the Bank. The following collateral requirements are in place to help ensure that the Bank remains in compliance with all statutes and regulations. Please direct any questions regarding the Bank’s collateral requirements to the Collateral Department at 800-357-3452 or email collateral@fhlbboston.com.

Collateral Requirements

Federal Housing Finance Agency regulations require that all extensions of credit from the Bank to members be fully secured by eligible collateral at all times. The regulations also identify the general types of assets the Bank may consider eligible collateral. Members are required to pledge eligible collateral to use the Bank’s products and solutions.

Eligible Collateral – Depository Institutions

Eligible collateral includes:

- Cash on deposit at the Bank that is specifically pledged to the Bank as collateral.

- Fully disbursed whole first-mortgage loans on improved residential real estate.

- Debt instruments issued or guaranteed by the U.S. government or any of its agencies.

- MBS issued or guaranteed by the U.S. government or any of its agencies

- Certain private-label MBS representing an interest in whole first-mortgage loans on improved residential real estate or commercial real estate.

- For community financial institutions only, small-business, small agri-business, and small-farm loans.

- In addition, under the Other Real Estate Related Category, other collateral types such as certain home-equity loans, home-equity lines of credit, first-mortgage loans on commercial real estate, and certain commercial mortgage-backed and municipal securities may be considered by the Bank if such collateral:

- Has a readily ascertainable value;

- Can be reliably discounted to account for liquidation and other risk;

- Can be liquidated in due course, if necessary.

- In all instances, the Bank must be able to perfect its security interest in such collateral.

See Appendix A for detailed collateral eligibility guidelines.

Note: Contact the Collateral Department at 800-357-3452 or email collateral@fhlbboston.com for additional information regarding the pledging of eligible securities.

Eligible Collateral – Insurance Company Members

Eligible collateral includes:

- Cash on deposit at the Bank that is specifically pledged to the Bank as collateral.

- Fully disbursed whole first-mortgage loans on improved residential real estate.

- Debt instruments issued or guaranteed by the U.S. government or any of its agencies.

- MBS issued or guaranteed by the U.S. government or any of its agencies.

- Certain private-label MBS representing an interest in whole first-mortgage loans on improved residential real estate or commercial real estate.

- In addition, under the Other Real Estate Related Category, other collateral types such as first-mortgage loans on commercial real estate, and certain commercial mortgage-backed and municipal securities may be considered by the Bank if such collateral:

- Has a readily ascertainable value;

- Can be reliably discounted to account for liquidation and other risk; and,

- Can be liquidated in due course, if necessary.

- In all instances, the Bank must be able to perfect its security interest in such collateral.

See Appendix A for detailed collateral eligibility guidelines.

Eligible Collateral – Community Development Financial Institutions (CDFIs)

Eligible collateral includes:

- Cash on deposit at the Bank that is specifically pledged to the Bank as collateral.

- Fully disbursed whole first-mortgage loans on improved residential real estate.

- Debt instruments issued or guaranteed by the U.S. government or any of its agencies.

- MBS issued or guaranteed by the U.S. government or any of its agencies.

- In addition, under the Other Real Estate Related Category, other collateral types such as certain home-equity loans, home-equity lines of credit, first-mortgage loans on commercial real estate, and participation loans may be considered by the Bank if such collateral:

- Has a readily ascertainable value;

- Can be reliably discounted to account for liquidation and other risk; and,

- Can be liquidated in due course, if necessary.

- In all instances, the Bank must be able to perfect its security interest in such collateral.

See Appendix A for detailed collateral eligibility guidelines.

Note: Contact the Collateral Department at 800-357-3452 or email collateral@fhlbboston.com for additional information regarding the pledging of eligible securities.

Conditions to the Bank’s Acceptance of Collateral

In general, in order for the Bank to accept an asset as eligible collateral, the following conditions, among others, must be met:

- The asset must be owned by the member free and clear of all other liens or claims, including UCC filings and other pledge and security agreements.

- The asset must not have been in default within the most recent 12-month period, except that whole first-mortgage loans on owner-occupied one-to-four family residential property are eligible collateral, provided that the borrower is not in arrears by two or more payments.

- Mortgages and other loans are considered eligible collateral, regardless of delinquency status, to the extent that the mortgages or loans are insured or guaranteed by the U.S. government or agency thereof.

- The asset must not be classified as substandard, doubtful, or a loss by the member or the member’s regulatory authority or reported as troubled debt restructure.

- The asset must not be encumbered by private transfer fee covenants, including securities backed by such mortgages and securities backed by the income stream from such covenants ― except for certain allowed transfer fee covenants (contact the collateral staff if you have questions).

- The asset cannot secure indebtedness — including mortgages — on which any director, officer, employee, attorney, or agent of the member or of any Federal Home Loan Bank is personally liable.

- The asset must comply with the Subprime and Nontraditional Loan Guidelines as detailed in Appendix C.

A residential mortgage loan1 that is secured by the borrower’s primary residence or a private-label (non-agency) MBS comprised of any such loans will not be accepted as collateral if it meets one or more of the following criteria:

- The annual interest rate and/or points and fees charged for the loan exceed the thresholds of the Home Equity Ownership Protection Act of 19942 (HOEPA);

- The loan has been identified by a member’s primary federal regulator as possessing predatory characteristics;

- The loan includes prepaid, single-premium credit insurance;

- The loan is defined as a High-Cost Loan, Covered Loan, or Home Loan, generally categorized under one or more federal, state, or local laws as having certain potentially predatory characteristics;

- The loan includes penalties in connection with the prepayment of the mortgage beyond the early years of the loan; or

- The loan requires mandatory arbitration to settle disputes.

1. A “residential mortgage loan” is a mortgage loan secured by a one-to-four-family residential property. For the Bank’s purposes, the definition includes mortgage loans and home equity loans and open-ended home equity lines of credit, including those secured by junior liens.

2.The applicable thresholds are noted in Truth in Lending – Regulation Z -12 CFR 226.32.

The Bank reserves the right, in its sole discretion, to refuse to accept certain assets as collateral, including, without limitation, assets constituting eligible collateral.

Collateral Maintenance Level

The amount of collateral that a member is required to maintain with the Bank at all times is referred to as its collateral maintenance level. Unless otherwise specified in writing by the Bank to the member, a member’s collateral maintenance level is the aggregate amount of eligible collateral, as defined in this guide and accepted by the Bank, that has a valuation equal to the aggregate amount of the Bank’s extensions of credit to the member. When determining that a member has met its collateral maintenance level, the Bank applies a collateral valuation discount (haircut) to all eligible collateral based on the Bank’s analysis of the risk factors inherent in the collateral. The Bank reserves the right, in its sole discretion, to adjust collateral discounts applied.

In the event that the discounted value of a member’s eligible collateral pledged to the Bank becomes insufficient to satisfy the member’s collateral maintenance level, including, without limitation, due to market depreciation, loan amortization or loan payoffs, the member is required to pledge additional eligible collateral so that the aggregate amount of the member’s eligible collateral is sufficient to satisfy the collateral maintenance level.

All fees and costs incurred by the Bank in connection with its collateral requirements may be charged to the member. The specific types of eligible collateral, additional conditions to the Bank’s acceptance of collateral, and the related percentages of book value, market value, or unpaid principal (as applicable) applied to collateral are discussed in more detail in Appendix A to this guide.

Use of Custodians

If a member uses an approved third-party custodian to hold eligible collateral otherwise required to be delivered to the Bank, it must provide the Bank with a first-priority security interest by entering into a control agreement with the custodian and the Bank.

Collateral Pledging Requirements – Depository Institutions

The primary distinction in the Bank’s collateral requirements for depository members in a particular credit category is the degree of documentation the member provides the Bank for certain loan collateral.

All securities must be delivered to the Bank or an approved third-party custodian1, regardless of a member’s credit category.

With respect to loan collateral, members in Credit Category 1 may generally report (on at least a quarterly basis) summary totals on their Qualified Collateral Reports for owner-occupied one-to-four-family residential mortgage loans. All other loans must be listed.

Conversely, members in Credit Category 2 or higher must list all loans. In addition, members in Credit Category 3 or 4 must deliver to the Bank (or an approved third-party) all loan documentation required by the Bank2. The chart below summarizes the Bank’s requirements.

| Depository Institutions | Category 1 | Category 2 | Category 3 and Category 4 |

|---|---|---|---|

| One- to four-family owner- occupied residential mortgage loans | Report totals | List | List and Deliver |

| All other loans | List | List | List and Deliver |

| Securities | Deliver | Deliver | Deliver |

All loan-level listings shall be in a format approved by the Bank and delivered at least quarterly (or more frequently as determined by the Bank).

1. The Bank reserves the right, at any time, to require members that have delivered securities to an approved third-party custodian to deliver the securities instead to the Bank.

2. Delivery of loan collateral may also be required of members, regardless of credit status, if the Bank determines that a creditor has filed a UCC financing statement on all of a member’s assets or a significant percentage of a member’s collateral pledged to the Bank.

Member’s Specific Collateral Recordkeeping Requirements – Depository Institutions

Credit Category 1 Members:

- May use, commingle, encumber, or dispose of any portion of their collateral as long as: a) there has been no event of default under the member’s “Agreement for Advances, Collateral Pledge, and Security Agreement;” and b) the remaining eligible collateral accepted by the Bank still satisfies the collateral maintenance level.

- Agree to permit Bank personnel to conduct periodic on-site reviews to verify collateral pledged.

Credit Category 2 Members:

- Are required to segregate and label all loans pledged as “Collateral for the Federal Home Loan Bank of Boston.”

- May not commingle, encumber, or dispose of any collateral without the express written consent of the Bank.

- Agree to permit Bank personnel to conduct periodic on-site reviews to verify listed collateral that is pledged.

Credit Category 3 and Category 4 Members:

- Are required to deliver to the Bank or to a Bank-approved third-party custodian an amount of eligible collateral, acceptable to the Bank, sufficient to satisfy the collateral maintenance level along with any required assignment of collateral to the Bank.

- May not use, commingle, encumber, or dispose of collateral that has been assigned and delivered without the express written consent of the Bank.

- Are required to segregate on site and mark as property of the Bank all ancillary documents that pertain to collateral that has been delivered to the Bank.

- Are required to notify the Bank of the acceptance of proceeds from the repayment of notes pledged to the Bank as collateral. The Bank may require the delivery of an amount of collateral equal to the proceeds of the repayment of the notes into a collateral account to secure the member’s indebtedness to the Bank.

- Agree to permit Bank personnel to conduct periodic on-site reviews to verify listed collateral that is pledged.

Collateral Pledging Requirements – Insurance Company Members and Community Development Financial Institution (CDFI) Members

- Insurance companies and CDFIs are required to deliver to the Bank or to a Bank-approved third-party custodian an amount of eligible collateral acceptable to the Bank, sufficient to satisfy the collateral maintenance level, along with any required assignment of collateral to the Bank.

- May not use, commingle, encumber, or dispose of collateral that has been assigned and delivered without the express written consent of the Bank.

- Depending on the type and nature of collateral, the Bank may request, and the member shall provide pertinent information, which may include, for example, financial information and rent rolls on commercial properties.

- For loan collateral, we require that the member’s mortgage servicer agrees to recognize and that the member acknowledge the Bank’s security interest in the pledged loans and loan documents and its contingent rights to the loan cash flows. The member may use its current servicer with the approval of the Credit Department, subject to the servicer maintaining a satisfactory financial condition.

- Are required to notify the Bank of the acceptance of proceeds from the repayment of notes pledged to the Bank as collateral. The Bank may require the delivery of an amount of collateral equal to the proceeds of the repayment of the notes into a collateral account to secure the member’s indebtedness to the Bank.

Additional Collateral Requirements

The Bank reserves the right to take any and all actions to protect its security position, assure compliance with this guide, and safeguard members’ investment in the Bank. Such actions may include, but are not limited to, requiring the delivery of additional collateral, whether or not such additional collateral would be deemed eligible collateral pursuant to this guide, and requiring a member to complete further steps to perfect the Bank’s security interest in the members’ pledged collateral. At the request of the Bank, each member agrees to execute, deliver to the Bank, and/or record, as applicable, such instruments, assignments, and other documents and to take other actions to evidence, preserve, and/or protect the security interest of the Bank in the collateral.

Eligible Assets Held in a Real Estate Investment Trust (REIT), Passive Investment Company (PIC), and/or Security Corporation

Assets of a member that have been transferred to a REIT and/or PIC, or other separately incorporated subsidiary, typically do not constitute eligible collateral for the Bank’s purposes. However, in certain cases the Bank may allow a member to include such assets in its collateral pledge provided that: (i) with respect to a REIT or PIC, the subsidiary pledges assets that constitute eligible collateral on behalf of the member and (ii) with respect to a security corporation, the member pledges the stock certificate(s) that prove its ownership of the security corporation.

Borrowing capacity generated by security corporation assets will be limited to eligible securities. All assets of a security corporation must be safekept at the Bank, with separate accounts for eligible and ineligible securities, as applicable. Before pledging these assets as collateral, please contact the Collateral Department at 800-357-3452 or email collateral@fhlbboston.com.

Termination of Membership

- Any member that has submitted a letter of intent to withdraw from membership in the Bank may not borrow under any advances program with a maturity date beyond the effective date of the member’s withdrawal.

- When a member has submitted a letter of intent to withdraw from the Bank, any outstanding advances with maturities extending beyond the date of withdrawal are subject to immediate prepayment of principal and interest, as well as appropriate prepayment fees, either on or before the withdrawal date. In the event of an involuntary termination of membership, whether by merger, acquisition, regulatory action, or otherwise, the Bank may allow a nonmember to assume the outstanding advances of the former member. If the Bank allows the nonmember to assume the outstanding advances, these advances must be fully secured by qualified collateral delivered to the Bank.

- In the event of voluntary or involuntary termination of membership:

- If a member prepays an advance for which an option to prepay without a fee is not a feature, the Bank will charge the member a prepayment fee sufficient to render the Bank indifferent to the prepayment.

- If there are Letters of Credit outstanding, i) the withdrawing member must deliver qualified collateral to the Bank in the amount of the outstanding letters of credit, to be held until the letters of credit expire, ii) the withdrawing member must substitute a letter of credit from another financial institution, naming the Federal Home Loan Bank of Boston as the beneficiary, or iii) the beneficiary must surrender the Letters of Credit to the Bank for cancellation. Approval by the Bank is required for whatever option is taken.

Appendices

Appendix A – Eligible Collateral and Collateral Valuation

The assets listed below constitute the Bank’s overall eligible collateral types. Please refer to the Collateral Requirements section to see the collateral types that may be pledged by member type.

The Bank may refuse certain collateral or adjust collateral discounts or valuations based on:

- The financial condition of the member.

- The review of the overall quality and volatility of the value of the collateral pledged. We make this determination based on the result of onsite member collateral reviews and/or our risk analysis.

The Bank will determine market value for all types of collateral at its sole discretion and may determine to value collateral at the unpaid principal balance.

The following tables summarize the valuation that we generally apply for collateral purposes. The five categories of eligible collateral are cash, securities, residential first-mortgage loans, community financial institution (CFI) collateral, and other real estate-related collateral.

Non-Depository Members

Please note: Haircuts to securities collateral are higher for certain non-depository members. More specifically, all non-depository Community Development Financial Institution (CDFI) members and those insurance company members domiciled in states whereby the insurance commissioners would likely impose a stay on the Bank’s ability to liquidate collateral (“stay-risk states”). A “stay-risk state” is defined as a state where law gives the receiver/conservator and/or the court broad powers to settle the insolvent CDFI’s and insurance company’s affairs, which could result in the Bank, as secured creditor, being subjected to a stay or injunction delaying its ability to resort to its collateral or subject it to “voidable transfer” or similar challenge to its secured position. Please contact the Collateral Department at 800-357-3452 or email collateral@fhlbboston.com to determine the securities collateral discounts applicable to your institution.

Please contact the Collateral Department at 800-357-3452 or email collateral@fhlbboston.com if you have questions regarding eligible collateral.

Cash Collateral

| Eligible Collateral | Valuation |

|---|---|

| Cash | 100% of balance |

- Cash must be on deposit in a collateral account at the Bank

Securities

- All members are required to deliver to the Bank or to a Bank-approved third-party custodian all securities pledged as collateral.

- Members that use a Bank-approved third-party custodian must execute a “control agreement” with the custodian and the Bank. All pledged securities must be maintained in a segregated account under the Bank’s exclusive control and have daily pricing of market values available to the Bank. Note: The Bank may require members that use a third-party custodian to instead deliver these securities to the Bank at any time.

- A member that holds securities in a security corporation subsidiary may be allowed by the Bank to deliver as eligible collateral the stock certificate(s) that evidence its ownership of the security corporation subsidiary. If allowed, the member is required to safekeep the underlying securities with the Bank.

- The Bank does not accept as collateral derivatives of eligible securities that contain excessive interest-rate and/or other financial risk, including, but not limited to, interest-only or principal-only strips of securities, residual or “Z” tranches of collateralized mortgage obligations, Inverse Floaters, and/or bonds without principal priority (e.g., PAC -2). Strips of U.S. Treasury securities are accepted as collateral.

- The Bank does not accept as collateral securities that are backed by properties encumbered by private transfer fee covenants or securities backed by the income stream from such covenants ― except for certain allowed transfer fee covenants.

| Eligible Collateral | Valuation: Percent of Market Value |

|---|---|

| U.S. Government and Agency Securities (excluding GNMA, FNMA and FHLMC mortgage-backed securities (MBS)) | By remaining term to maturity 0<3 years: 98% 3<20 years: 95% 20<25 years 94% 25+ years: 93% |

| U.S. Government and Agency STRIPS | By remaining term to maturity 0<3 years: 98% 3<15 years: 95% 15<20 years: 94% 20<25 years 92% 25+ years: 91% |

| GNMA, FNMA and FHLMC MBS, and Agency CMOs | By structure Floating Rate (under rate cap): 98% Pass-Through: 96% CMO/Agency CMBS: 95% GNMA HECM Bonds: 98% |

| Eligible Collateral | Valuation: Percent of Market Value |

|---|---|

| U.S. Government and Agency Securities (excluding GNMA, FNMA and FHLMC mortgage-backed securities (MBS)) | By remaining term to maturity 0<3 years: 90% 3<5 years: 87% 5<8 years: 84% 8<10 years: 79% 10<15 years: 72% 15<20 years: 65% 20<25 years: 60% 25+ years: 56% |

| U.S. Government and Agency STRIPS | By remaining term to maturity 0<3 years: 90% 3<5years: 87% 5<8 years: 81% 8<10 years: 79% 10<15 years: 69% 15<20 years: 61% 20<25 years: 54% 25+ years: 50% |

| GNMA, FNMA and FHLMC MBS, and Agency CMOs | By structure Floating Rate (under rate cap): 96% Pass-Throughs, by remaining term: <10 years: 86% 10<20 years: 82% 20 years+: 79% Residential CMO: 77% Agency CMBS: 73% GNMA HECM Bonds: 92% |

| Eligible Collateral | Valuation: Percent of Market Value |

|---|---|

| Non-Agency Residential MBS1 | 50% of market value |

| Securities representing an equity interest in collateral eligible for advances2 | Valuation is determined in accordance with the applicable underlying assets. |

1. Limited to AAA-rated securities. Borrowing capacity limited to 20% of the amount of the member’s GAAP capital. Must represent an unsubordinated interest in whole first-mortgage loans on improved residential property. All underlying mortgage loans are subject to certain eligibility requirements for residential loans, as outlined in this guide. Private placement securities must be issued under rule 144A.

2. Must represent an undivided equity interest in underlying assets of a security corporation subsidiary.

Residential First-Mortgage Loans

Definition of Owner-Occupied Principal Residence: Loans secured by owner-occupied dwellings. An owner-occupied dwelling is the borrower’s primary residence. First lien owner-occupied residential loans are included in this section. (Second liens on owner-occupied residences are included in other real estate-related collateral.)

Definition of Non-Owner-Occupied Residence: Second homes, vacation homes, or other investor-type properties. These loans must be listed. First liens on non-owner-occupied loans are included in this section. Please note: Second liens on non-owner-occupied residences are not eligible as collateral.1

Other Eligibility Guidelines

- Eligible residential first-mortgage loan collateral that becomes subject to a superior lien, including, but not limited to, tax liens, mechanics liens, UCC filings, or any other encumbrance, loses its eligibility.

- Eligible residential first-mortgage loan collateral must not be delinquent by two or more payments.

- Eligible residential first-mortgage loan collateral may not be classified as substandard, doubtful, or loss by the member or by its regulator, or reported as troubled debt restructuring.

- Eligible residential first-mortgage loan collateral may not include loans to officers, directors, employees, attorneys, or agents of the member institution or the Bank.

- Eligible residential first-mortgage loan collateral must not be encumbered by private transfer fee covenants ― except for certain allowed transfer fee covenants (contact the collateral staff if you have questions).

- Eligible residential first-mortgage loan collateral with loan-to-value (LTV) ratios over 90% (with the exception of Loans insured under Title II of the National Housing Act, i.e., insured by the FHA) must have private mortgage insurance.

- Residential first-mortgage loan collateral with loan-to-value (LTV) ratios over 100% (with the exception of loans insured under Title II of the National Housing Act, i.e., insured by the FHA) are not eligible as collateral.

- Loans must fully comply with either or both, as applicable, the Interagency Guidance on Nontraditional Mortgage Product Risks issued by the FFIEC on October 4, 2006, and/or the Statement on Subprime Mortgage Lending Risks dated July 10, 2007, to be eligible as collateral.

- Loans that allow for negative amortization of the principal balance, including pay-option adjustable-rate mortgage loans, and home equity conversion mortgages (also known as “reverse mortgages”) are not eligible as collateral.

- Loans for which the borrower’s ability to service the debt is not evidenced by written documentation may only be pledged if the member is providing the Bank with loan-level data for all pledged residential one- to four-family loan collateral.

- Loans that meet the Bank’s definition of both a subprime and nontraditional loan may only be pledged if the member is providing the Bank with loan-level data for all pledged residential one- to four-family loan collateral.