For nearly 95 years, FHLBank Boston has served as a trusted partner to its members, helping to foster economic growth and stability across the region by providing reliable wholesale funding and liquidity. In 2025, FHLBank Boston maintained its ongoing commitment to serve member financial institutions, helping them advance affordable housing and economic development throughout New England. FHLBank Boston and the FHLBank System’s efforts were highlighted on a national scale in late 2025 when independent research from the Urban Institute revealed that the FHLBanks deliver $13.2 billion to $21.4 billion in annual economic value by serving as a critical liquidity backstop that strengthens bank stability, reduces systemic risk, and helps prevent bank failures during periods of financial stress.

Learn more about how FHLBank Boston supports New England by reading this report and viewing the short video below. See perspectives from FHLBank Boston President & Chief Executive Officer Timothy J. Barrett, Board Member and bankESB Chief Strategy Officer William M. Parent, and Advisory Council Vice Chair and Maine Housing Director Dan Brennan.

The Bank had a really good year in 2025. We saw a steady activity from our members. We saw some focus in our residential mortgage activities, our MPF activities. Members were very in tune to the change in administration, the change in the regulatory environment, so we spent a lot of time educating them as to what the impact would be at our Bank.

We also engaged with our members in a way I think this year more than even previous years. We’re out in the community quite a bit. Our HCI team was out to all the states. Our board was out to two states this year. We’re going to continue that next year.

The outreach that the Federal Home Loan Bank does with their partners and other organizations is among the more robust that I have seen in my travels. They are constantly on the road. They are constantly engaging. They do a very good job at listening and hearing what the various diverse needs of New England are.

2025 was another stellar year. I think it was the top five year of earnings, and therefore that money gets allocated to our affordable housing programs. 10% goes to our statutory AHP, and this year in 2025, we were able to give at least another 10% to our voluntary programs.

The Federal Home Loan Bank System is a catalyst working with our member banks by providing funding, programs, and advances to member banks so that they can help with construction and really go at creating a larger stock of housing availability in New England.

We’ve been in a situation in New England where housing costs are rising dramatically faster than incomes are. The uniqueness of the programs is the impact they have on people that are most in need. The programs help those that are struggling, help those that need that one extra step to get into their first home, get into an affordable apartment. And they have a direct impact on that. And when they do that, the Bank succeeds, the Bank is fulfilling its mission.

We use the Home Loan Bank to offer down-payment assistance of over $3 million to first-time homebuyers. We also use the MPF Program to sell over $30 million of loans. By offering and having access to sell loans to the Federal Home Loan Bank, it offers an opportunity to actually provide even more credit to homebuyers in our communities.

It’s also worth mentioning that the Bank increased its on-balance sheet liquidity position for our members. We’re at a position now where a lot of our lending is sourced through this on-balance sheet liquidity. We have great access to the markets. We can continue to borrow money to meet the needs of our members, but in 2025 we saw a dramatic increase of on-balance sheet liquidity that provides easy access to our members in any economic cycle.

What makes small businesses confident that they can get access to their money in an efficient way and also provides members the opportunity to provide them credit and leverage so that they can grow their businesses, they can invest in their communities. That’s a really critical and important overall role that we play at the Federal Home Loan Bank as a catalyst for the New England economy overall.

Looking ahead in 2026, we’re going to build on the success of 2025. We have some aggressive goals to continue to expand our lending, especially with insurance companies and in the MPF market. We look forward to engaging even more with our members. We’re going to visit all the states again this year, and the board’s on the road as well. And we look forward to another great year.

The Bank increased its on-balance sheet liquidity position for our members. We’re at a position now where a lot of our lending is sourced through this on-balance sheet liquidity. We have great access to the markets. We can continue to borrow money to meet the needs of our members.

Timothy J. Barrett

President, Chief Executive Officer

FHLBank Boston

Our Mission

The mission of the Federal Home Loan Bank of Boston is to provide highly reliable wholesale funding and liquidity to member financial institutions throughout New England. We strive to deliver the best financial products, services, and expertise that support home financing, affordable housing, and community development, including programs targeted to lower-income households.

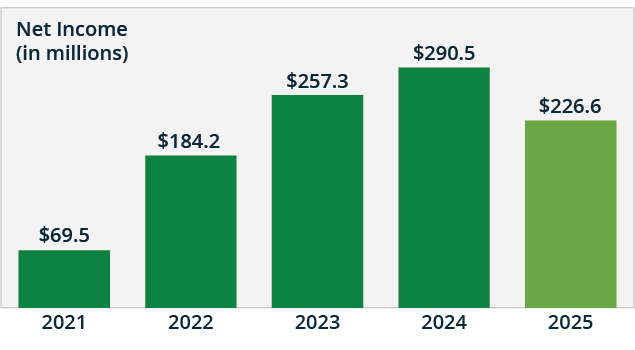

In 2025, FHLBank Boston’s financial results were shaped by changing interest rate conditions and member demand for advances. Member utilization of the Mortgage Partnership Finance® (MPF®) Program grew significantly. Additionally, the Bank contributed $32.6 million to the Affordable Housing Program and $31.4 million for affordable housing and community investment programs like Housing Our Workforce, Lift Up Homeownership, Jobs for New England, the CDFI Advance program, and the MPF Permanent Rate Buydown product.

Net income was $226.6 million in 2025, a $63.9 million decrease from $290.5 million in 2024. The drop in income was driven primarily by a decrease of $56.2 million in net interest income after provision for credit losses, and an increase of $11.1 million in discretionary housing and community investment programs expense and voluntary Affordable Housing Program contributions.

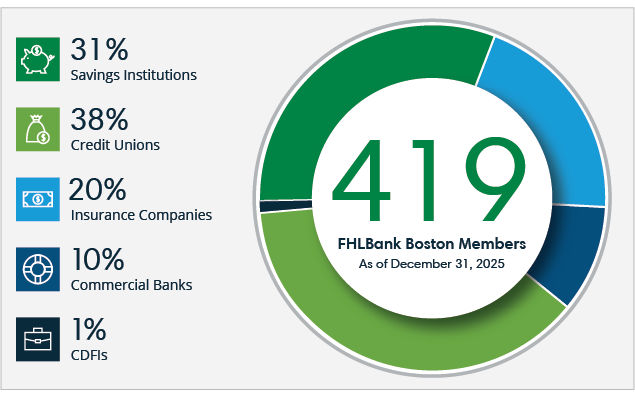

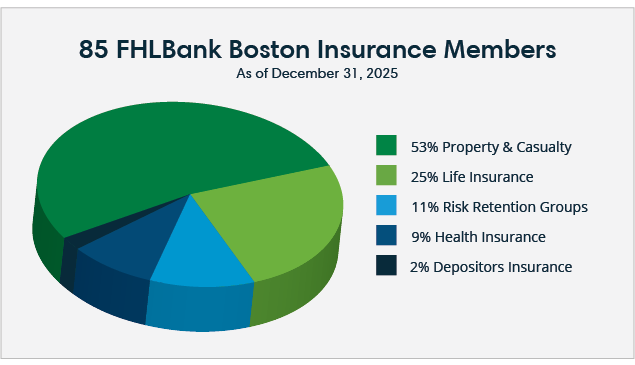

FHLBank Boston’s membership is comprised of banks, credit unions, insurance companies, and Community Development Financial Institutions of varying sizes. We view our members as partners to whom we provide access to reliable funding and experts to help them with strategic solutions for managing interest-rate volatility, reducing funding costs, optimizing mortgage funding, and supporting communities’ economic development and affordable housing needs. We welcomed nine new members in 2025: six insurance companies, two credit unions, and one bank.

Odyssey Reinsurance Company is pleased to be a member of Federal Home Loan Bank Boston. This relationship represents an important part of our financial and investment strategy as it enables us to access a strong, flexible source of liquidity.

Richard F. Coerver IV

Executive Vice President, Chief Financial Officer Odyssey Reinsurance Company (member since 2024)

Members relied on a range of FHLBank Boston financial products and solutions to help them strengthen and support their communities in 2025. FHLBank Boston’s flexible offerings include advances, a secondary-market mortgage program, and letters of credit. The offerings can be tailored to allow members to address specific needs in a changing economic environment and maintain their commitment to serving New England communities. The MPF Permanent Rate Buydown product, launched in 2024 and offered again in 2025, provided mortgage rates up to 2% below market for 243 lower-income borrowers. See below for more on the product’s impact.

Advances

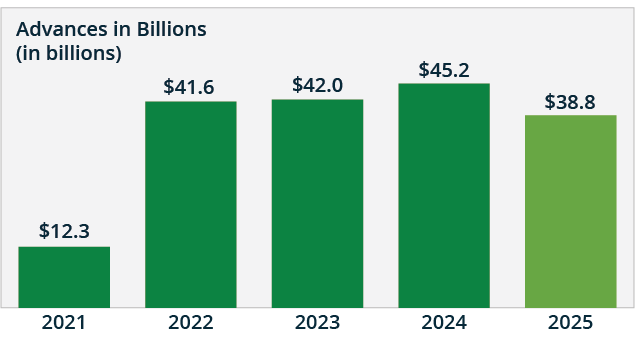

In 2025, advances helped members manage a shifting rate environment. Markets moved from “higher for longer” expectations to gradual cuts, while volatility remained elevated and the yield curve stayed uneven. Members leveraged advances as a way to stay nimble when rate paths were unclear.

FHLBank Boston advances are a planned, readily available, and flexible funding tool that helps keep our balance sheet nimble. Advances have evolved into a core liquidity and asset-liability management strategy that we view as supportive, and as we take actions to adjust to shifting economic conditions.

Bob Morgan

Chief Executive Officer

NorthCountry Federal Credit Union

Mortgage Partnership Finance®

Members can use the MPF Program to increase balance-sheet liquidity and improve profitability. By selling eligible loans into the program, members can support growth in priority assets and avoid concentrating long-term assets on their own balance sheet. Due to growing interest in the Program, the MPF team expanded in 2025 to better serve members. Also, the Permanent Rate Buydown (PRB) product continued to attract members by offering up to a 2% reduction in mortgage interest rates for eligible borrowers, those earning up to 80% of the area median income. Members delivered 243 loans to PRB in 2025, with 78% of those being first-time homebuyers.

Coastal1’s participation in the 2025 Permanent Rate Buydown program through FHLBank Boston allows us to deliver immediate, long-term affordability to our borrowers by lowering the interest rates from day one. This creates meaningful monthly savings and makes homeownership a more attainable goal for families in our community. The program is a powerful tool that aligns with both our core values of ‘People Helping People’ and our lending strategy, creating a lasting impact for the members we serve.

Kevin Farrell

Chief Lending Officer

Coastal1 Credit Union

“Mortgage Partnership Finance” and “MPF” are registered trademarks of the Federal Home Loan Bank of Chicago.

Letters of Credit

FHLBank Boston’s Letters of Credit (LOCs) continued to provide members with a flexible, cost-effective alternative to pledging securities. Members used LOCs to back deposits from state and municipal entities, provide credit support for taxable and tax-exempt bonds, and guarantee contractual performance on their own behalf and on behalf of customers. This allowed members to unencumber high-quality securities, improve balance-sheet liquidity metrics, and better align their asset-liability management strategies while maintaining and growing important municipal and public-sector relationships.

Profile Bank has been a longtime user of the FHLBank Boston’s Letters of Credit (LOCs). It is a cost effective, user-friendly way to easily collateralize our local and state government deposits. Their Online Banking platform makes it efficient with retained beneficiary details, and also automatically emails the LOCs to our customers. The icing on the cake is the ease of acceptance by the beneficiaries, as they already know the strength of the FHLBank System.

Kevin Miller

President, Chief Executive Officer

Profile Bank

Community Impact

Across FHLBank Boston, employees share a commitment to creating meaningful impact for our New England-based members and communities. Through active participation in volunteer initiatives connected with FHLBank Boston’s mission, such as organizations that promote financial literacy, hunger relief, support for local homelessness and poverty relief efforts, among many others, employees make a meaningful difference.

We demonstrate our commitment to the community through volunteering and developing partnerships with nonprofit organizations aligned with our mission.

Amy Iseppi

Vice President, Director of Government and Community Relations

FHLBank Boston

Mission Led

Like our members, FHLBank Boston employees are committed to making a positive impact in New England. The Bank supports mission-aligned nonprofit organizations through sponsorships and employee volunteer opportunities. In 2025, these efforts included partnerships with organizations such as Habitat for Humanity, Boston Area Gleaners, St. Francis House, Pine Street Inn, Women’s Lunch Place, Bridge Over Troubled Waters, and Christmas in the City, among others. In addition, FHLBank Boston collaborated with local organizations, including the Massachusetts Bankers Association and the Boston City Council, to provide educational programming for employees.

Boston Area Gleaners

Volunteers gathered surplus crops and packed them for donation to food banks, pantries, community kitchens, and other food-access initiatives.

Women’s Lunch Place

Bank employees helped kitchen staff at the Women’s Lunch Place to prepare healthy and delicious breakfasts and lunches for women who are experiencing homelessness or trauma in their lives.

Women & Allies Business Resource Group Build for Habitat for Humanity

The Bank’s Women & Allies Business Resource Group chose to use a volunteer day to help build a new residence in Cohasset, Massachusetts, for Habitat for Humanity.

Massachusetts Bankers Association

FHLBank Boston sponsored the Massachusetts Bankers Association’s Women & Allies in Banking Conference, which was attended by Bank employees.

Catie’s Closet

Catie’s Closet gives children access to clothing and basic necessities so they can thrive in school and life. Bank volunteers helped sort clothing by size, gender, and type so it can be distributed to those who need it most.

A Conversation with Boston City Council President

The Bank hosted an event with Boston City Council President Ruthzee Louijeune called “All Politics is Local.” It was attended by many in the Bank, including President, Chief Executive Officer Timothy J. Barrett, who is pictured with Louijeune above.

Winter Walk

Employees joined more than 3,000 walkers for the Winter Walk to fight homelessness and support Bridge Over Troubled Waters, an organization that assists homeless and at-risk youth.

Intern Build for Habitat for Humanity

Bank interns came together to help build a Habitat for Humanity home.

Christmas in the City

FHLBank Boston sponsored backpacks and volunteered for Christmas in the City to support Boston-area families experiencing homelessness and poverty.

Advisory Council Report

Affordable Housing Program

The Affordable Housing Program (AHP) turned 35 years old in 2025. Since its beginning, the program has supported the creation or preservation of 40,089 affordable homes. In 2025 alone, direct subsidy support, combined with low-interest funding, helped create or preserve 23% more affordable homes in New England than the previous year. Forty-nine initiatives serving low- and moderate-income individuals, families, seniors, those with disabilities, and formerly homeless people benefited from AHP funding. Watch the video below to hear how a Maine bank and local partner have benefited from the program and learn more about this important program’s impact on the New England economy.

Transcript

We’re in need of housing. There’s no question, and affordability is a real challenge for many. For more than 20 years now, I’ve been working with the Federal Home Loan Bank and the AHP program. The program is helping us to create more housing in our communities.

The Affordable Housing Program is a capital grant and interest rate subsidy program specifically designed to build affordable rental and homeownership housing for low- to moderate-income individuals and households. One of the things I love about our program is that this is private capital funding. It’s generated through the Bank’s earnings. So, this isn’t a public subsidy that’s governed by a different process. This is actually the Bank putting its money where its mouth is.

Before the pandemic, the Affordable Housing Program really was valuable in helping Maine Housing spread their limited resources around the state and build more affordable housing. Since the pandemic, it’s become critical to helping us address the steep rise in construction costs.

What it effectively does is it buys down the interest rate from current market rates. We’re generally seeing a 2 to 3% discount on the rate. When you have a 40-unit apartment building that was very costly to build, if it had just all traditional debt structured against it, that would be a real cost burden, and you’d have to have higher rents to be able to support all of the costs. By minimizing the cost of the debt payment after the traditional operating costs, you can now offer those lower rents.

AHP has had a significant impact in New England, from veterans’ housing to special needs housing to homeless housing to cooperatives to seniors’, manufactured housing. We’ve seen it all over the 35 years of the program. The money has facilitated the development of over 40,000 homes throughout New England. These are real people, these are teachers, firefighters, civil service workers that are living in affordable, safe, decent homes to support their lives.

Federal Home Loan Bank of Boston is an amazing partner. They’re very flexible, they always work with us. They also bring their funding in earlier in the projects, helping us leverage funds and make our dollars stretch farther. It’s an amazing partnership, and we couldn’t do what we do without the Federal Home Loan Bank of Boston.

It’s been exciting to work with the Federal Home Loan Bank and be a part of so many of these.

Developers in the affordable housing sector are tremendously committed, passionate about their work. It’s uplifting and motivating.

I’ve been in this for close to 30 years now, and there’s nothing more satisfying than going to a ribbon cutting or a dedication, and people are so grateful and so thankful that the Bank was able to provide a grant because they now have a place to live. Nothing makes you feel better than that.

The money has facilitated the development of over 40,000 homes throughout New England. These are real people. These are teachers, firefighters, civil service workers that are living in affordable, safe, decent homes to support their lives.

Kenneth Willis Senior Vice President, Director of Housing & Community Investment

FHLBank Boston

Affordable Housing Program Data

2025 Low-Interest Advances

$12,770,883

2025 Grants & Subsidies

$34,249,501

2025 Affordable Housing Intiatives

49

2025 Affordable Homes

1,532

1990-2025 Low-Interest Advances

$365,271,886

1990-2025 Grants & Subsidies

$463,988,184

1990-2025 Affordable Housing Initiatives

1,384

1990-2025 Affordable Homes

40,089

State

Awards

Number of Projects

*Number of Units

CT

$4,096,307 in grants, loans, and interest-rate subsidies

3

125

ME

$15,185,271 in grants, loans, and interest-rate subsidies

12

375

MA

$20,334,913 in grants, loans, and interest-rate subsidies

24

616

NH

$378,892 in grants, loans, and interest-rate subsidies

1

6

RI

$1.7 million in grants

2

158

VT

$2,975,000 in grants

4

124

*Number of affordable units lists is as reported by members; number of units refers to affordable units only.

Connecticut

110 Washington, Hartford, Massachusetts Housing Investment Corporation, Boston Communities, Arch Communities LLC, 57 rental units, $750,000 grant

Church Street Commons, Hebron, Liberty Bank, NDC Housing and Economic Development Corporation, Commons Community Development Corporation, 48 rental units, $850,000 grant

Dresser Woods, Salisbury, Torrington Savings Bank, Salisbury Housing Committee, Inc., 20 rental units, $1,196,307 grant and subsidy, $1.3 million loan

Maine

Belmont Avenue Apartments, Belfast, Bangor Savings Bank, Waldo Community Action Partners, 40 rental units, $850,000 grant

Quebec Commons, Biddeford, Maine Community Bank, Westbrook Development Corporation, Westbrook Housing Authority, 40 rental units, $1,199,822 grant and subsidy, $1,200,000 loan

Varney Heights, Freeport, Bath Savings Institution, Freeport Housing Trust, Inc., 42 rental units, $749,842 grant

Winter Street Apartments, Lisbon, Norway Savings Bank, Realty Resources Development LLC, Coastal Affordable Housing, 42 rental units, $980,930 grant and subsidy, $350,000 loan

Harding Family Homes, Orland, Bangor Savings Bank, Homeworkers Organized for More Employment, 6 rental units, $390,000 grant

Cumberland Housing, Portland, Bath Savings Institution, Portland Housing Authority, Portland Housing Development Corporation, 40 rental units, $1,194,897 grant and subsidy, $1.2 million loan

Mayo Housing, Portland, Norway Savings Bank, Portland Housing Authority, Portland Housing Development Corporation, 27 rental units, $1,197,009 grant and subsidy, $12 million loan

Prosperity Place, Portland, Maine Community Bank, ProsperityME, Developers Collaborative, 50 rental units, $850,000 grant

School Street Apartments, Saco, Bangor Savings Bank, Quality Housing Coalition, 7 rental units, $455,000 grant

Stratton Court, Scarborough, Maine Community Bank, South Portland Housing Development Corporation, South Portland Housing Authority, 43 rental units, $1,199,116 grant and subsidy, $1.2 million loan

Meeting House Hill Apartments, Waldoboro, Bangor Savings Bank, Volunteers of America, Northern New England, Inc., 36 rental units, $850,000 grant

Duplex Condo 3 Carrean, Waterville, First National Bank, Waterville Community Land Trust, 2 homeownership units, $119,360 grant

Massachusetts

416 Great Road, Acton, All One Credit Union, Habitat for Humanity North Central Massachusetts, Inc., 3 homeownership units, $900,000 grant

Pequoig House, Athol, The Bank of Canton, Fairview Housing Partners, EJR Health LLC, 11 CTL LLC, 53 rental units, $850,000 grant

25 Bridge Street, Boston, Eastern Bank, Bridge Over Troubled Waters, 64 rental units, $850,000 grant

7-9 Westminster Terrace, Boston, Eastern Bank, Planning Office for Urban Affairs, Inc., Roxbury Stone House, Inc., 13 rental units, $500,000 grant

Visions of Victory, Boston (Jamaica Plain), Eastern Bank, Victory Programs, Inc., 41 rental units, $850,000 grant

250 Seaver Street, Boston, Eastern Bank, The Commonwealth Land Trust, Inc., 16 rental units, $978,796 grant and subsidy, $980,000 loan

Brewster 3571 Main St. Community Housing, Brewster, Cape Cod Five Cents Savings Bank, Habitat for Humanity of Cape Cod, Inc., 2 homeownership units, $180,000 grant

Evergreen Circle, Erving, Greenfield Savings Bank, Rural Development, Inc., 26 rental units, $1,197,009 grant and subsidy, $1.2 million loan

Fairmont St. Projects, Fitchburg, Rockland Trust Company, Making Opportunity Count, Inc., 42 rental units, $850,000 grant

Birch Street Greenfield, Greenfield, Greenfield Co-Operative Bank, Pioneer Valley Habitat for Humanity, Inc., 1 homeownership unit, $75,000 grant

The Winslow PSH Preservation, Greenfield, Greenfield Savings Bank, Greenfield Housing Associates, Inc., 55 rental units, $200,000 grant

Massachusetts (continued)

Essex County Habitat 512 Washington Street Affordable Housing, Haverhill, Institution for Savings in Newburyport and its Vicinity, Essex County Habitat for Humanity, 7 rental units, $420,000 grant

Prosperity Way Stage Two, Housatonic (Great Barrington), Adams Community Bank, Central Berkshire Habitat for Humanity, 7 homeownership units, $630,000 grant

Tahattawan Road Littleton, Littleton, All One Credit Union, Habitat for Humanity North Central Massachusetts, Inc., 2 homeownership units, $70,000 grant

Broadway Supportive Housing II, Lowell, Eastern Bank, Common Ground Development Corporation, 37 rental units, $500,000 grant

5 Auburn Street, Natick, Eastern Bank, Metro West Collaborative Development, Inc., 32 rental units, $1,198,198 grant and subsidy, $3,440,883 loan

Linden Terrace Phase One A LLC, Needham, Citizens Bank, Affordable Housing and Services Collaborative, Inc., Peabody Housing LLC, 76 rental units, $850,000 grant

27 Crafts Ave., Northampton, Greenfield Savings Bank, Valley Community Development Corporation, 30 rental units, $850,000 grant

Bellevue Veterans Community, Oak Bluffs, Rockland Trust Company, Island Housing Trust Corporation,12 rental units, $800,000 grant

BC Arc VII Shaker Lane, Pittsfield, Pittsfield Co-Operative Bank, Berkshire County Arc, Inc., 4 homeownership units, $250,000 grant

Essex County Habitat for Humanity Homeowner Initiative Wenham, Wenham, Institution for Savings in Newburyport and its Vicinity, Essex County Habitat for Humanity, 2 homeownership units, $180,000 grant

Poland and Streeter Schools Redevelopment, Winchendon, Fidelity Co-Operative Bank, Montachusett Veterans Outreach Center, Incorporated, 44 rental units, $891,712 grant and subsidy, $500,000 loan

Colony on Grove, Worcester, Massachusetts Housing Investment Corporation, Colony Retirement Homes, Inc., Affirmative Investments, 45 rental units,$850,000 grant

521-523 Sunderland Rd., Worcester, Beacon Bank & Trust, Habitat for Humanity – Metrowest/Greater Worcester Inc., 2 homeownership units, $133,000 grant

New Hampshire

Kingston Veterans Residence, Kingston, Newburyport Five Cents Savings Bank, Housing Support, Inc., 6 rental units, $178,892 grant and subsidy, $200,000 loan

Rhode Island

160 Broad Street Apartments, Providence, Centreville Bank, Crossroads Rhode Island, 97 rental units, $850,000 grant

183 Washington/Preservation, West Warwick, Citizens Bank, Women’s Development Corporation, 61 rental units, $850,000 grant

Vermont

Three 33 Jones, Brandon, Bar Harbor Bank and Trust, Housing Trust of Rutland County, Inc., 29 rental units, $425,000 grant

Chalet Apartments, Brattleboro, Citizens Bank, Evernorth, Inc, Windham & Windsor Housing Trust, 31 rental units, $850,000 grant

Faywood Road, Grand Isle, Union Bank, Evernorth, Inc., Cathedral Square Corporation, 24 rental units, $850,000 grant

Newport Crossing, Newport, Community National Bank, Gilman Housing Trust, Inc., 40 rental units, $850,000 grant

Initiatives Outside of New England

Cleveland West Veterans Housing, Cleveland, Ohio, Citizens Bank, CHN Housing Partners, 62 rental units, $850,000 grant

Drueding Center Residential, Philadelphia, Pennsylvania, Citizens Bank, Drueding Center, 26 rental units, $850,000 grant

Winter West Affordable, Philadelphia, Pennsylvania, Citizens Bank, Philadelphia Chinatown Development Corporation, 40 rental units, $650,000 grant

Homeownership Assistance Programs

Buying a home remained challenging in New England for many households in 2025 due to elevated mortgage interest rates and high home prices. However, FHLBank Boston’s three down-payment assistance programs continued to help first-time homebuyers and borrowers with incomes below 80% of the area median income, as well as those earning more than 80% and up to 120% of the area median income, purchase homes. Liberty Bank in Connecticut has consistently used the programs to assist homebuyers with varying incomes. By engaging in FHLBank Boston’s homeownership assistance programs, Liberty Bank has delivered measurable, positive outcomes, promoting its mission to improve the lives of its customers and communities.

Liberty Bank’s use of FHLBank Boston’s programs for down-payment and closing cost assistance has enabled our borrowers to overcome upfront cost barriers and achieve sustainable homeownership. By leveraging high-impact grants like FHLBank Boston’s Equity Builder Program, Housing Our Workforce, and their Lift Up grant, our loan officers consistently maximize FHLBank Boston’s programs to support as many of our qualified borrowers as possible. These programs not only strengthen affordability for our customers but also enhance our community lending mission by directing meaningful financial support to households across a wide range of income levels.

Fanita Borges

First Vice President

Liberty Bank

Equity Builder Program

In 2025, the Equity Builder Program (EBP), helped 139 more buyers purchase their first home than the prior year. Homeowners with incomes up to 80% of the area median income used EBP grants for down payments, closing costs, and rehabilitation expenses.

Equity Builder Program Data

2025 Grants Committed

$7,017,784

2025 Member Participants

70

2025 Homebuyers

282

2003-2025 Grants Committed

$69,082,962

2003-2025 Member Participants

190

2003-2025 Homebuyers

5,023

Connecticut

American Eagle Financial Credit Union

Charter Oak Federal Credit Union

Connex Credit Union

CorePlus Federal Credit Union

First County Bank

Liberty Bank

Newtown Savings Bank

Northwest Community Bank

Thomaston Savings Bank

Torrington Savings Bank

Webster Bank, N.A.

Windsor Federal Bank

Maine

Bangor Savings Bank

Katahdin Federal Credit Union

Katahdin Trust Company

Kennebec Savings Bank

Maine Savings Federal Credit Union

Massachusetts

Adams Community Bank

Athol Credit Union

bankESB

bankHometown

Bay State Savings Bank

BayCoast Bank

Beacon Bank & Trust

Bluestone Bank

Cambridge Savings Bank

Cape & Coast Bank

Cornerstone Bank

Dean Co-Operative Bank

Dedham Institution for Savings

East Cambridge Savings Bank

Eastern Bank

Fall River Five Cents Savings Bank

Fidelity Co-Operative Bank

Greenfield Co-Operative Bank

Greylock Federal Credit Union

Harvard Federal Credit Union

Institution for Savings in Newburyport and its Vicinity

Leader Bank, N.A.

Lee Bank

Mechanics Cooperative Bank

Metro Credit Union

Millbury Federal Credit Union

MountainOne Bank

North Shore Bank, A Co-Operative Bank

Northern Bank & Trust Company

PeoplesBank

Pittsfield Co-Operative Bank

Rockland Trust Company

Salem Five Cents Savings Bank

St. Mary’s Credit Union

The Bank of Canton

The Cooperative Bank

Winter Hill Bank, FSB

New Hampshire

Bellwether Community Credit Union

Claremont Savings Bank

Mascoma Bank

Sugar River Bank

Rhode Island

BankNewport

Centreville Bank

Citizens Bank, N.A.

The Washington Trust Company

Vermont

Community National Bank

EastRise Federal Credit Union

Green Mountain Credit Union

National Bank of Middlebury

NorthCountry Federal Credit Union

Passumpsic Savings Bank

Union Bank

Vermont Federal Credit Union

*State reflects members’ headquarters. Some members on this list disbursed grants in more than one state.

Housing Our Workforce

Housing Our Workforce increased its down-payment assistance by more than $2.2 million in 2025, committing $7,320,021 to households earning more than 80% and up to 120% of the area median income. In the last year, 296 households received assistance from the program.

Housing Our Workforce Data

2025 Grants Committed

$7,320,021

2025 Member Participants

73

2025 Homebuyers

296

2019-2025 Grants Committed

$25,378,246

2019-2025 Member Participants

112

2019-2025 Homebuyers

1,284

Connecticut

American Eagle Financial Credit Union

Charter Oak Federal Credit Union

Chelsea Groton Bank

Connex Credit Union

Dime Bank

First County Bank

Liberty Bank

Newtown Savings Bank

Northwest Community Bank

Webster Bank, N.A.

Windsor Federal Bank

Maine

Bangor Savings Bank

Bar Harbor Bank and Trust

Bath Savings Institution

Katahdin Federal Credit Union

Katahdin Trust Company

Kennebec Savings Bank

Maine Community Bank

Maine Savings Federal Credit Union

Norway Savings Bank

University Credit Union

Massachusetts

Adams Community Bank

Athol Credit Union

bankESB

bankHometown

Bay State Savings Bank

BayCoast Bank

Bluestone Bank

Cambridge Savings Bank

Cape & Coast Bank

Cornerstone Bank

Dean Co-Operative Bank

Dedham Institution for Savings

East Cambridge Savings Bank

Eastern Bank

Fall River Five Cents Savings Bank

Fidelity Co-Operative Bank

Greenfield Co-Operative Bank

Greenfield Savings Bank

Greylock Federal Credit Union

Harvard Federal Credit Union

Haverhill Bank

Institution for Savings in Newburyport and its Vicinity

Leader Bank, N.A.

Metro Credit Union

North Easton Savings Bank

North Shore Bank, A Co-Operative Bank

Pentucket Bank

PeoplesBank

Pittsfield Co-Operative Bank

Rockland Trust Company

Salem Five Cents Savings Bank

St. Mary’s Credit Union

The Bank of Canton

The Cooperative Bank

Webster Five Cents Savings Bank

Winter Hill Bank, FSB

New Hampshire

Bellwether Community Credit Union

Claremont Savings Bank

Mascoma Bank

Salem Co-Operative Bank

Rhode Island

BankNewport

Centreville Bank

Citizens Bank, N.A.

The Washington Trust Company

Vermont

Community National Bank

EastRise Federal Credit Union

Green Mountain Credit Union

National Bank of Middlebury

NorthCountry Federal Credit Union

Northfield Savings Bank

Union Bank

Vermont Federal Credit Union

*State reflects members’ headquarters. Some members on this list disbursed grants in more than one state.

Lift Up Homeownership

The Lift Up Homeownership program helped 149 first-generation homebuyers with down-payment and closing-cost assistance in 2025. To qualify for the program, all homebuyers must have incomes up to or below 120% of the area median income, and the homebuyer must also certify that the parents and/or legal guardian of at least one borrower does not currently own a home in the United States and has not previously owned a home in the United States, or at least one borrower has aged out of foster care.

Lift Up Homeownership Data

2025 Grants Committed

$7,320,021

2025 Member Participants

39

2025 Homebuyers

149

2023-2025 Grants Committed

$14,820,021

2023-2025 Member Participants

49

2023-2025 Homebuyers

304

Connecticut

American Eagle Financial Credit Union

First County Bank

Liberty Bank

Newtown Savings Bank

Northwest Community Bank

Thomaston Savings Bank

Webster Bank, N.A.

Windsor Federal Bank

Maine

Bangor Savings Bank

Katahdin Trust Company

Massachusetts

Adams Community Bank

bankESB

BankFive (legal name is Fall River Five Cents Savings Bank)

bankHometown

Bay State Savings Bank

BayCoast Bank

Bluestone Bank

Cambridge Savings Bank

Cape & Coast Bank

Cornerstone Bank

Eastern Bank

Fidelity Co-Operative Bank

Greenfield Co-Operative Bank

Greylock Federal Credit Union

Leader Bank, N.A.

Lee Bank

Metro Credit Union

Pittsfield Co-Operative Bank

Rockland Trust Company

Rollstone Bank & Trust

Salem Five Cents Savings Bank

St. Mary’s Credit Union

The Bank of Canton

Rhode Island

BankNewport

The Washington Trust Company

Vermont

EastRise Federal Credit Union

Green Mountain Credit Union

Union Bank

Vermont Federal Credit Union

*State reflects members’ headquarters. Some members on this list disbursed grants in more than one state.

Community Development Advance

Member use of the Community Development Advance (CDA) Program increased in 2025, contributing to the development or preservation of 113% more housing units and 26.3% more economic development or mixed-use initiatives than in 2024. This discounted financing program was used by members to support a range of initiatives, including the preservation of nine income-restricted rental units in Boston, the redevelopment of a courthouse into 46 new affordable rental units in Central Falls, Rhode Island, and the construction of 47 apartments for tenants with incomes at or below 80% of the area median income in Terryville, Connecticut.

Community Development Advance Program Data

2025 Advances

$739,287,953

2025 Housing Units

1,041

2025 Economic Development or Mixed-Use Initiatives

72

1990-2025 Advances

$24,062,702,166

1990-2025 Housing Units

128,320

1990-2025 Economic Development or Mixed-Use Initiatives

2,009

This investment helps protect homes, strengthen families, and preserve affordability in a neighborhood facing real displacement pressure. By partnering with FHLBank Boston, we are keeping Naturally Occurring Affordable Housing in our region and ensuring that the buildings are leased to an organization providing critical transitional housing. This is what impact looks like when mission-driven capital meets local leadership.

Moddie Turay

President, Chief Executive Officer

Massachusetts Housing Investment Corporation

Community Development Financial Institution Advance

The Community Development Financial Institution (CDFI) Advance program strengthens partnerships between members and non-depository CDFIs. It supports the development of affordable housing, job creation and small business growth, and the expansion of community facilities in distressed New England communities. In two years since the program began, FHLBank Boston provided $50.9 million in advances and $11.5 million in subsidies to 28 member institutions, which were directed to support programs of local CDFIs.

Community Development Financial Institution Advance Data

2025 Advances

$26,556,075

2025 Subsidy

$6,953,262

2025 Participating Members

22

2024-2025 Advances

$50,906,075

2024-2025 Subsidy

$11,527,304

2024-2025 Participating Members

28

Our partnership with FHLBank Boston is a true collaboration that enables us to fulfill our mission of supporting community-based enterprises.

Gina Maroni

Senior Vice President, Chief Financial Officer

UMassFive College Federal Credit Union

From Pop Up to Permanence

When Wooden Cooperative – a worker-owned restaurant and bakery based in Worcester, MA – sought capital in 2025 for renovations, retail expansion, and equipment purchases to scale its food service and baking production, its cooperative ownership structure made traditional financing unavailable. Recognizing this challenge, Wooden Cooperative’s Community Development Financial Institution partner, Cooperative Fund of the Northeast (CFNE), reached out to UMassFive College Federal Credit Union.

UMassFive College Credit Union, an FHLBank Boston member, applied for an interest-free advance through the CDFI Advance program to deliver the capital needed to bring the project to fruition.

“UMassFive was proud to underwrite a loan to CFNE and facilitate more of their work. Our partnership with FHLBank Boston is a true collaboration that enables us to fulfill our mission of supporting community-based enterprises,” said Gina Maroni, senior vice president and CFO of UMassFive College Federal Credit Union.

Wooden Cooperative, formerly known as Wooden Noodle, is a worker-owned restaurant and bakery established in 2018 as a pop-up concept. The enterprise transitioned to a permanent cooperative restaurant in 2021. Subsequently, it merged with an existing bakery, significantly expanding both production and retail capacity. In 2024, the cooperative comprised six worker-owners and 21 employees, generating $693,000 in combined revenue from the restaurant and bakery.

To support its continued growth, Wooden Cooperative partnered with CFNE, which provides financing and technical assistance to cooperatives and employee-owned businesses in the northeast.

CFNE provided a $35,000 revolving line of credit, which enabled Wooden Cooperative to complete required buildout improvements associated with a $75,000 City of Worcester forgivable equipment grant.

The project strengthened and stabilized operations, preserving and creating quality jobs within a democratic, worker-owned model. In addition, the cooperative offers affordable commercial space to local artisans and emerging food entrepreneurs, fostering small business incubation and contributing to Worcester’s local food ecosystem. Located within a CDFI-qualified investment area, Wooden Cooperative plays a meaningful role in advancing inclusive economic development, workforce opportunity, and community-based ownership.

Baked goods on display at Wooden Cooperative in Worcester, MA.

Jobs for New England

Jobs for New England (JNE) supports economic development across New England by helping members assist local small businesses that create and preserve jobs in their communities. With JNE’s below-market-rate financing, members can provide low-cost loans to help businesses purchase needed equipment, upgrade facilities, and expand. Since the program’s inception in 2016, JNE has supported the creation or preservation of 15,260 jobs.

Jobs for New England Data

2025 Advances

$32,361,986

2025 Subsidy

$5,410,700

2025 Participating Members

44

2025 Jobs Created/Preserved

1,526

2016-2025 Advances

$396,734,357

2016-2025 Subsidy

$44,595,467

2016-2025 Participating Members

110

2016 Jobs Created/Preserved

15,260

*Job numbers as reported by members.

Union Bank’s $140,000 Jobs for New England Advance for Pie Fixes Everything, LLC (Poorhouse Pies) supported equipment purchases and renovations for a second location. At least nine jobs will be added, including two executive chefs. The new large production kitchen will enable the business to meet the demand for pies, donuts, and full-service catering. Owner, Suzanne Tomlinson (a/k/a Pie Lady), expects to nearly double revenues and provide a small seating area for patrons and community members to socialize.

Rebecca (Becky) Stebbins

Assistant Vice President, Commercial Loan Officer

Union Bank

Grants for New England Partnerships

The Grants for New England Partnerships program reflects FHLBank Boston’s commitment to banks and credit unions to help strengthen local communities. In 2025, $25,000 grants were awarded to 10 members who supported 14 local nonprofit organizations, including those focused on affordable housing, people with mental health challenges, and places providing shelter for domestic violence survivors.

Grants for New England Partnerships Data

2025 Grants

$25,000

2025 Members

10

2025 Nonprofit Organizations

14

Grants for New England Partnerships Recipients

Member

Nonprofit Organization

Aroostook County Federal Savings & Loan Association

Homeless Services of Aroostook

Bank of New Hampshire

NeighborWorks Southern New Hampshire

Berkshire Bank

The Urban League of Greater Hartford

Cambridge Savings Bank

Greater Lowell Family YMCA

Kennebunk Savings Bank

Fair Tide

Mascoma Bank

Vermont Community Loan Fund

Massachusetts Housing Investment Corporation

Housing Corporation of Arlington

Merrimack County Savings Bank

Marguerite’s Place

Merrimack County Savings Bank

Overcomers Refugee Services

Merrimack County Savings Bank

Family Promise of Southern New Hampshire

Merrimack County Savings Bank

National Alliance on Mental Illness New Hampshire (NAMI New Hampshire)

Merrimack County Savings Bank

The Granite YMCA

MHIC, LLC

The Neighborhood Developers, Inc.

Partners Bank

Sanford-Springvale YMCA

At Bank of New Hampshire, we are dedicated to partnerships that make a meaningful difference in the communities we have proudly served for over 194 years. We are honored to select NeighborWorks Southern New Hampshire for FHLBank Boston’s Grants for New England Partnerships program, recognizing the vital work they do to improve financial stability for individuals and families in southern New Hampshire. Their mission aligns closely with our commitment to building stronger, more resilient communities and supporting local families in need of safe, affordable housing.

FHLBank Boston looks to the future of housing with the Affordable Housing Development Competition. Graduate students collaborate with sponsors and mentors to create practical, community-focused housing proposals that bridge academic theory and industry practice. Marking its 25th year, the 2025 competition drew seven entries from students with interests in architecture, real estate, planning, finance, and policy. Winning proposals included a multi-purpose one- and two-bedroom residential living facility for seniors and live-in caregivers in South Boston; a community of single-room occupancy units, studios, and two-bedroom units for hospitality industry workers in Jay, Vermont; and the transformation of a half-acre lot in Putney, Vermont, into six affordable homeownership units. Learn more about the competition’s 25-year history in the video below.

Transcript

Housing is the biggest issue locally, statewide, and nationally. It affects our economy, it affects how people live, it affects their opportunities for schooling, for employment.

The Affordable Housing Development Competition connects graduate students from a variety of different universities and colleges with a nonprofit developer. Over a course of about six and a half to seven weeks, they take a project that’s in that developer’s pipeline and develop a very comprehensive proposal that includes detailed renderings, development budgets, timeline, and more.

As the sponsor, we get a really talented team of Boston area students who will evaluate the site as we would do as developers. To have that quality proposal, to be able to show all of the financial stakeholders and elected officials and city government and neighbors, that this is a real potential use for the site, and that’s what makes the competition so valuable to a nonprofit sponsor.

We’re working with students from UMass Boston, Harvard, MIT, the Boston Architectural Collaborative, to Clark, Wentworth, and UMass Amherst. We have proposals from all over New England. We have downtown Boston. We have Northern Maine. We have Connecticut. We have Martha’s Vineyard. There is a need for affordable housing everywhere.

The work to develop affordable housing is so complex. You’re working with so many different kinds of people in different disciplines, whether it’s in city government, state government, banks. All of those pieces have to come together, and the students get to see exactly how that works.

Hearing from students saying that this has been the most valuable experience in their graduate school career has really been like super affirming for me and rewarding but also knowing that we really are helping to create that next generation of affordable housing professionals.

I’ve hired students. I know they’ve been hired by my peer community development organizations and other developers of affordable housing. It’s fun to see some of the affordable housing development competition students as they launch their careers around Boston.

Most meaningful to me in the work we’re doing with the Bank and the competition is ensuring that going forward, we have people committed to affordable housing that know how to make it happen. It’s a win-win situation for the community, the developer, and the students.

We’ve been so fortunate to have great sponsors who come back year after year, and we really couldn’t do it without all of them at the table helping to support the effort. Kudos to the Bank for having brought the concept of this competition through fruition and created an event that can withstand 25 years.

Knowing that we really are helping to create that next generation of affordable housing professionals is rewarding.

Tobi Goldberg

Sr. Community Investment Manager

FHLBank Boston

2025 Winning Proposals

The Mosaic South Boston, MA

First Place: $10,000 – The Mosaic aims to convert South Boston High School into 83 units of low-income senior housing and residential community spaces, including a rooftop garden, games and arts room, fitness center, and large multipurpose space.

Workforce Modu-Lodge Jay, VT

Second Place: $7,000 – Workforce Modu-Lodge provides a flexible mix of modular-construction single-room occupancy units, studios, and two-bedroom units in Jay for seasonal and year-round workers in the hospitality industry.

Eva Mondon Commons Putney, VT

Third Place: $4,000 – Eva Mondon Commons is intended to transform a half-acre rural Vermont lot into six affordable homeownership units.

Housing Competition Sponsors

Federal Home Loan Bank of Boston

Boston Society for Architecture

CohnReznick LLP

Kuehn Charitable Foundation

ICON Architecture, Inc.

Citizens’ Housing and Planning Association

Our Leaders

The leadership team is anchored by the Management Committee and board of directors, which consist of member directors elected by members in each of the six New England states, as well as independent directors nominated by the board. Board directors use their expertise in financial services, housing and community development, real estate, and cybersecurity to guide the Bank’s strategic priorities, oversee the budget and key policies, and ensure the safety and soundness of operations. The management committee and board are advised by the 15-member Advisory Council, comprising housing and development leaders focused on the Affordable Housing Program and community investment.

Edward F. Manzi, Jr. (Retired September 2025) Chairman, Chief Executive Officer Fidelity Cooperative Bank Leominster, MA

John C. Witherspoon (Vice Chair) Director Skowhegan Savings Bank Kingfield, Maine

Kevin D. Miller President, Chief Executive Officer Profile Bank Rochester, New Hampshire

Duncan Barnard Chief Internal Auditor CLS Bank New York, New York

William M. Parent Chief Strategy Officer bankESB Quincy, Massachusetts

Donna L. Boulanger Director North Brookfield Savings Bank North Brookfield, Massachusetts

David Rotatori President, Chief Executive Officer Ion Bank Naugatuck, Connecticut

Michael A. Brown Rear Admiral, United States Navy (Ret.) Retired Cybersecurity Executive Seabrook, New Hampshire

E. Macey Russell Retired Law Partner Newton, Massachusetts

Caroline R. Carpenter President, Chief Executive Officer National Bank of Middlebury Middlebury, Vermont

Robert Tourigny Executive Director NeighborWorks Southern New Hampshire Manchester, New Hampshire

Thomas J. Curry Retired Law Partner and Bank Regulator Osterville, Massachusetts

Gregg C. Tumeinski Executive Vice President, Chief Financial Officer The Beacon Mutual Insurance Company Warwick, Rhode Island

Antoinette C. Lazarus Vice President, Compliance Conning Hartford, Connecticut

Executive Committee

Chairman:

Eric Chatman

Vice Chairman:

John C. Witherspoon

Committee Chairs:

Duncan Barnard

*Caroline R. Carpenter

Thomas J. Curry

Antoinette C. Lazarus

Kevin D. Miller

William M. Parent

E. Macey Russell

Audit Committee

Chair:

Duncan Barnard

Vice Chairman:

*William M. Parent

Committee:

Antoinette C. Lazarus

Kevin D. Miller

Robert Tourigny

Finance Committee

Chair:

Kevin D. Miller

Vice Chairman:

David Rotatori

Committee:

Duncan Barnard

Michael A. Brown

John C. Witherspoon

Governance/Government Relations Committee

Chair:

Thomas J. Curry

Vice Chairman:

Antoinette C. Lazarus

Committee:

Donna L. Boulanger

Kevin D. Miller

Robert Tourigny

John C. Witherspoon

Housing & Community Development Committee

Chair:

E. Macey Russell

Vice Chairman:

Robert Tourigny

Committee:

Michael A. Brown

Caroline R. Carpenter

Thomas J. Curry

Gregg Tumeinski

Human Resources & Compensation Committee

Chair:

Antoinette C. Lazarus

Vice Chairman:

Thomas J. Curry

Committee:

Donna L. Boulanger

William M. Parent

E. Macey Russell

John C. Witherspoon

Risk Committee

Chair:

*Caroline R. Carpenter

Vice Chair:

*David Rotatori

Committee:

Donna L. Boulanger

E. Macey Russell

Gregg Tumeinski

Technology Committee

Chair:

William M. Parent

Vice Chair:

Michael A. Brown

Committee:

Duncan Barnard

Caroline R. Carpenter

David Rotatori

Gregg Tumeinski

Council of Federal Home Loan Banks

Timothy J. Barrett

Eric Chatman

John C. Witherspoon

The chair of the Board is an ex-officio member of all committees of the Board. However, the chair is not counted in determining the number of committee members necessary to constitute a quorum; but, if present, the chair is counted for purposes of establishing a quorum at any such committee meeting and is entitled to vote unless otherwise provided in a committee’s charter.

*Assumed additional board leadership responsibilities upon Edward F. Manzi’s retirement.

Daniel Brennan (Chair) Director Maine State Housing Authority Augusta, Maine

Katherine Easterly Martey Executive Director New Hampshire Community Development Finance Authority Concord, New Hampshire

Jeanne Cola (Vice Chair) Executive Director Local Initiatives Support Corporation – Rhode Island Providence, Rhode Island

Joshua R. Meehan Executive Director Keene Housing Keene, New Hampshire

Elizabeth Bridgewater Executive Director Windham & Windsor Housing Trust Brattleboro, Vermont

Cathy Mercado Executive Director Merrimack Valley Housing Partnership Lowell, Massachusetts

Rodger L. Brown Jr. Managing Director of Real Estate Development Preservation of Affordable Housing, Inc. Boston, Massachusetts

Sharon Morris Executive Director Omni Development Corporation Providence, Rhode Island

Maura Collins Executive Director Vermont Housing Finance Agency Burlington, Vermont