Advance Solutions for Funding Construction Lending

Tyler Buckeridge

Utilizing advances for construction loans can keep interest-rate and liquidity risks manageable and align funding with the characteristics of the loans.

Funding the Construction Lifecycle

FHLBank Boston advances can sit alongside deposits and other wholesale sources to align term, repricing, and liquidity with the loan’s evolution.

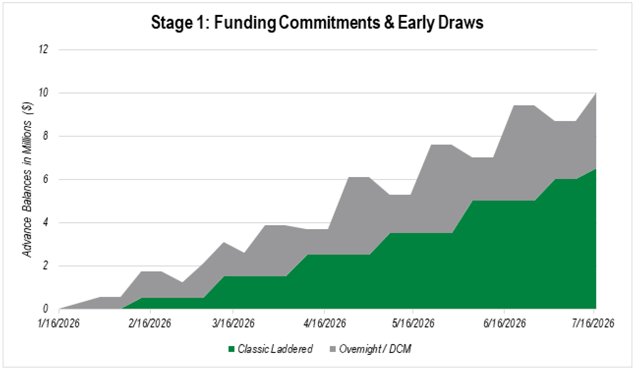

Commitments and Early Draws: Funding the Ramp, Not Just the Peak

Construction facilities typically start as large, undrawn or lightly drawn commitments. As usage builds, funding needs follow.

Institutions may wish to:

- Estimate a base level of expected usage over the coming quarters based on historical draw patterns and project budgets.

- Fund that base with term funding—such as a ladder of shorter-term Classic Advances—Reserve the Daily Cash Manager (DCM) Advance and other very short-term funding for day-to-day fluctuations above that base level.

This type of approach can:

- Help lock in more predictable pricing for the portion of construction balances expected to be outstanding for more than a few days, and

- Keep overnight and very short-term funding focused on operational liquidity rather than structural ramps in construction usage.

The chart below illustrates funding a “base” with Classic laddered Advances and using Overnight/DCM as a buffer for draw-timing variability.

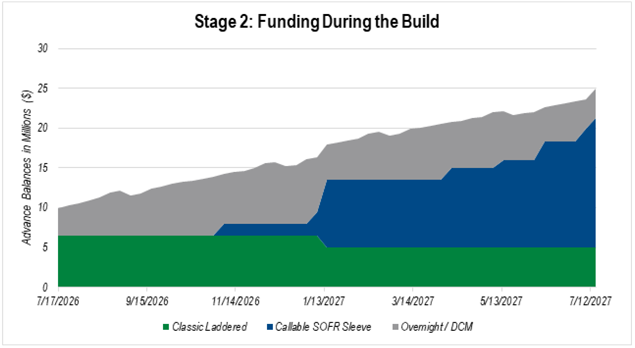

During the Build: Managing Rate and Liquidity Risk

During active construction, balances tend to grow, and the loan coupon often floats. At this stage, funding tools that can help align asset and liability behavior include:

Callable SOFR-Indexed Floater Advance

- May pair naturally with floating or frequently repricing construction notes (priced off SOFR plus a spread).

- Callable features can provide optionality when paydowns, sales, or take-outs occur earlier than expected.

- Example structure: A six-month maturity, three-month lockout, one-x call (“six-month NC3 (one-x )”) gives the member a six-month final maturity and the ability to pay it down at the three-month mark with no prepayment fee, if desired. Pricing floats at Overnight SOFR + 18 bps; if Overnight SOFR is 3.70% on day one, the initial rate would be 3.88% (rates shown are illustrative and change daily.)

- Can help lock in a fixed cost of funds while preserving flexibility to shorten the funding if a project pays down, sells, or refinances earlier than expected (after the call-protection period).

- May be considered when there is meaningful prepayment or sale uncertainty, but term funding is preferred to routinely rolling large balances in very short-term sources.

In practice, many institutions may lean toward one primary “core” tool in this stage based on their broader balance-sheet positioning—often Callable SOFR-indexed Floater Advances for asset-sensitive balance sheets, or a fixed-rate Member-Option slice for more liability-sensitive profiles. If construction balances pay down, deposits arrive stronger than expected, or other assets (e.g., investments) prepay and free up cash, these structures—and DCM—can help resize wholesale funding without friction.

As shown below, as balances become durable, the mix may shift toward Callable SOFR and/or Member-Option Advances to align repricing and reduce reliance on daily roll.

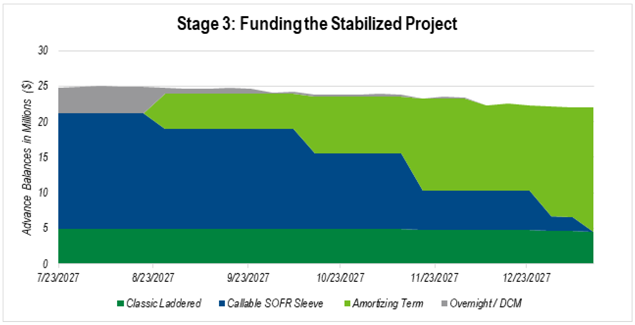

Once a project is complete, the funding need shifts from bridging construction to supporting a mini-perm or term CRE position—or to bridging to an anticipated external take-out.

Stabilization and Take-Out: Bridging to the Long Term

Once a project is complete, the funding need shifts from bridging construction to supporting a mini-perm or term CRE position—or to bridging to an anticipated external take-out.

Depending on the strategy for the asset, institutions may consider:

Longer-term Classic Advances or Amortizing Advances

- Longer-term Classic Advances or Amortizing Advances can be structured to mirror the expected maturity and, in the case of amortizing structures, the loan’s scheduled principal payments.

- This approach can help align funding cash flows with the underlying loan and reduce the need to refinance funding in the middle of the expected asset life.

- Members can often choose an amortization pace that fits their balance-sheet needs—faster or slower—depending on cash-flow expectations, liquidity preferences, and overall interest-rate risk posture.

Shorter fixed-rate or callable structures

- When a sale or external refinancing is expected on a defined horizon, favoring shorter maturities or longer advances with member-controlled options to shorten (Discount Note Auction-Floater or Member-Option Advance) may be used to bridge to that expected take-out.

- These structures can provide term funding today with a clearer path to repayment around the planned disposition.

In all cases, the objective is to avoid a multi-year asset funded primarily with a sequence of very short-term borrowings and instead use advances to better align term, repricing, and expected cash flows with the construction and mini-perm life cycle.

After stabilization, funding often transitions to longer-term and amortizing structures, with Overnight/DCM declining toward zero, as shown in the graph below.

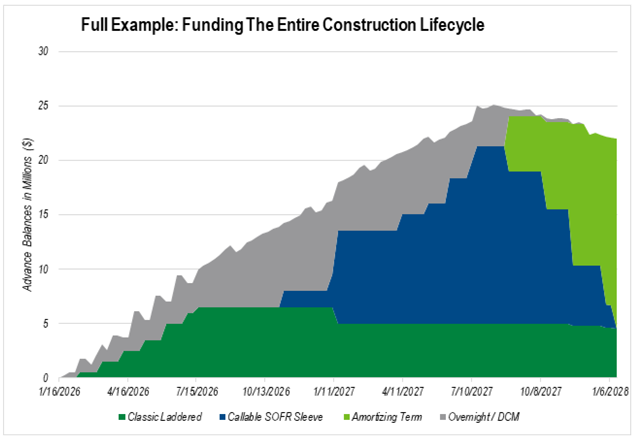

Example: Funding a $25 Million Mixed-Use Project

The concepts above can be illustrated with a simplified example of a $25 million mixed-use construction project in New England.

Commitment and Ramp

- The facility is approved as a $25 million construction/mini-perm structure, and outstanding balances ramp unevenly, reaching ~$10 million by month six.

- The institution funds the expected “base” portion of early usage with a ladder of shorter-term Classic Advances (shown as a single Classic bucket in the chart). By month six, the Classic ladder totals ~$6.5 million, while DCM / overnight is used as the flexible buffer for draw timing variability (about $3.5 million at month six).

During Construction

- As balances continue to build beyond the initial ramp, the institution begins shifting a growing portion of funding into Callable SOFR-Indexed Floater Advances, so funding remains closely tied to the floating index on the construction note. Depending on broader balance-sheet sensitivity and rate-certainty preferences, some institutions may instead use a fixed-rate Member-Option slice or a blend. Example structure: six-month NC3 (1x) Callable SOFR, priced at Overnight SOFR + 18 bps.

- By month 12, the project is around $18 million outstanding, funded with roughly $13.5 million in longer-term tools and $4.5 million DCM (about 25% overnight).

Stabilization and Term

- At peak construction usage around month 18, balances reach ~$25 million, with overnight funding used primarily as a buffer (~15% in the scenario).

- As the project stabilizes and transitions toward a mini-perm/term CRE structure, the institution replaces a meaningful portion of floating construction-stage funding with a longer-term Amortizing Advance, structured to pay down systematically alongside expected principal payments (and potentially faster/slower depending on balance-sheet preferences).

- By month 24 (stabilized), the balance is ~$22 million and funded 100% longer-term in the scenario (DCM essentially drops to zero).

Viewed over time, the mix between overnight and term funding might look like this for the same project:

| Time Point | Outstanding Balances | Share in Overnight Advances | Share in Longer-Term Advances |

|---|---|---|---|

| Month 0 | $0MM | 0% | 0% |

| Month 6 | $10MM | 35% | 65% |

| Month 12 | $18MM | 25% | 75% |

| Month 18 | $25MM | 15% | 85% |

| Month 24 (Stabilized) | $22MM | 0% | 100% |

A simplified example of how the funding mix can evolve from early draws through peak construction and stabilization is shown in the graph below.

How This Funding Approach Shows Up in Risk Measures

A construction funding framework built around these stages and tools can be easier to integrate into existing risk views:

- Rate Risk: Across the project lifecycle, using a combination of floating or fixed-rate advances to fund construction balances can help keep asset and liability repricing broadly aligned.

- Liquidity Risk: Incorporating expected draw patterns into internal liquidity views—together with available FHLBank Boston borrowing capacity and pledged collateral—can clarify how advances might support future usage without relying solely on day-to-day market conditions.

Flexible Funding for Construction Lending

Whether the focus is infill multifamily, mixed-use, or owner-occupied facilities, construction lending tends to work best when the funding plan is as clear as the credit structure. FHLBank Boston’s Financial Strategies group can help translate a construction pipeline into an advance-funding approach that considers commitments, draws, and take-outs, and aligns collateral so capacity is available when needed.

For more information, please contact me at tyler.buckeridge@fhlbboston.com or connect with your relationship manager.

FHLBank Boston does not act as a financial advisor, and members should independently evaluate the suitability and risks of all advances. The content of this article is provided free of charge and is intended for general informational purposes only. FHLBank Boston does not guarantee the accuracy of third-party information displayed in this article, the views expressed herein do not necessarily represent the view of FHLBank Boston or its management, and members should independently evaluate the suitability and risks of all advances.

Forward-looking statements: This article uses forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 and is based on our expectations as of the date hereof. All statements, other than statements of historical fact, are “forward-looking statements,” including any statements of the plans, strategies, and objectives for future operations; any statement of belief; and any statements of assumptions underlying any of the foregoing. The words “expects”, “may”, “likely”, “continue”, “possible”, “to be”, “will,” and similar statements and their negative forms may be used in this article to identify some, but not all, of such forward-looking statements. The Bank cautions that, by their nature, forward-looking statements involve risks and uncertainties, including, but not limited to, the uncertainty relating to the timing and extent of FOMC market actions and communications and economic conditions (including effects on, among other things, interest rates and yield curves). The Bank reserves the right to change its plans for any programs for any reason, including but not limited to legislative or regulatory changes, changes in membership, or changes at the discretion of the board of directors. Accordingly, the Bank cautions that actual results could differ materially from those expressed or implied in these forward-looking statements, and you are cautioned not to place undue reliance on such statements. The Bank does not undertake to update any forward-looking statement herein, or that may be made from time to time on behalf of the Bank.

As a Sales & Strategies Specialist, Tyler applies his analytical skills and data-driven insights to support FHLBank Boston members and enhance their understanding of how the Bank’s products and services can help them achieve their performance goals.