Securing Public Deposits Without Tying Up the Balance Sheet

Tyler Buckeridge

Public deposits can be an important source of relationship funding, but how they are secured can affect liquidity, earnings, and balance sheet flexibility. FHLBank Boston letters of credit offer a way to provide required credit support while preserving more flexibility across the balance sheet.

The Hidden Balance Sheet Cost of Public Deposit Collateral

Public deposits can help banks and credit unions diversify funding, deepen municipal relationships, and support a broader community banking strategy. But they often come with a practical requirement: the deposits may need to be secured.

For many financial institutions, that has historically meant pledging investment securities. That approach can work, but it can also create tradeoffs. Once securities are pledged to support public deposits, they may no longer be available for liquidity, sale, borrowing, or broader portfolio management. In some cases, collateral requirements may also influence what the institution owns in the securities portfolio.

For institutions managing liquidity, loan growth, securities portfolio positioning, and municipal relationships simultaneously, the collateral strategy for public deposits can be just as important as the deposit rate.

Letters of credit (LOCs) from FHLBank Boston may provide another approach. In a public deposit context, an LOC can provide credit support to the depositor while allowing the member to use eligible collateral pledged to FHLBank Boston, rather than tying up investment securities directly with the depositor or custodian. For institutions managing liquidity, loan growth, securities portfolio positioning, and municipal relationships simultaneously, the collateral strategy for public deposits can be just as important as the deposit rate.

Releasing Securities and Preserving Liquidity

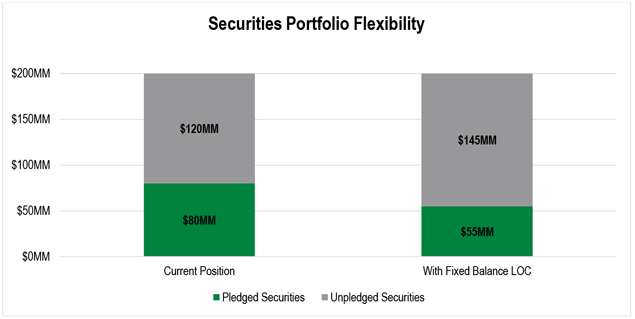

Consider a hypothetical $1 billion institution with $200 million in securities, of which $80 million is currently pledged to support public deposit relationships. In this example, the institution instead uses a $25 million FHLBank Boston Fixed Balance LOC to replace a portion of the securities pledged directly to support those deposits.

The balance sheet does not get larger. The public deposit relationship is still supported. But the collateral approach changes.

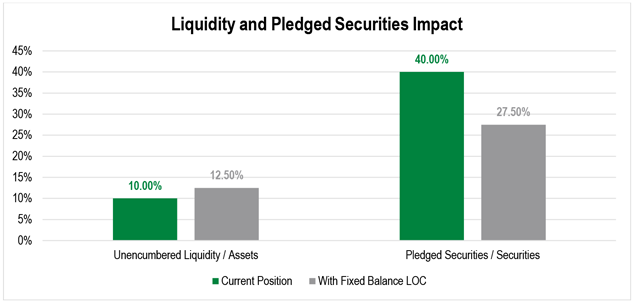

Before the LOC, the scenario assumes $100 million of unencumbered liquidity, equal to 10.00% of total assets. Separately, the institution has $200 million in securities, of which $80 million is pledged to support public deposits and $120 million is unpledged.

After replacing $25 million of the direct securities pledge with an LOC, securities previously pledged to support public deposits are released from that specific pledge arrangement. Assuming the LOC is supported by sufficient existing eligible collateral capacity at FHLBank Boston, the released securities may increase the scenario’s unencumbered liquidity measure to $125 million, or 12.50% of total assets.

The securities pledge math is straightforward: pledged securities decline from $80 million to $55 million, while unpledged securities increase from $120 million to $145 million. As a share of the securities portfolio, pledged securities fall from 40.00% to 27.50%.

The same shift can also make the securities portfolio more flexible by increasing the portion of the portfolio that is not pledged directly to public deposit relationships. That gives the institution more securities available for liquidity, portfolio management, or other balance sheet needs.

That improvement comes with a tradeoff. The LOC uses FHLBank Boston borrowing capacity. In this simplified example, the institution starts with $200 million of remaining borrowing capacity; using a $25 million LOC reduces that capacity to $175 million. The increase in on-balance sheet liquidity flexibility should be evaluated alongside the effect on remaining borrowing capacity.

The Earnings Tradeoff

The liquidity benefit is only part of the analysis. Institutions should also consider whether pledging requirements are influencing asset allocation.

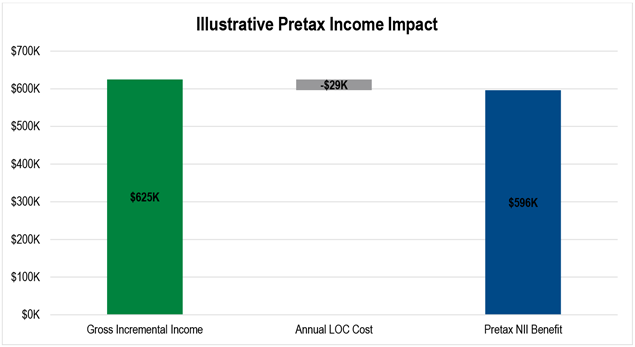

In the same example, assume the institution had been holding $25 million in securities yielding 3.25% primarily to support public deposit collateral needs. If the use of a LOC allows the institution to redeploy that same $25 million into loans or other earning assets yielding 5.75%, the gross income pickup is 250 basis points.

That spread creates $625,000 of additional annual income. Assuming a one-yearFixed Balance LOC fee of 11.5 basis points, the annual LOC cost would be approximately $28,750. In this example, the pretax net interest income benefit would be approximately $596,250.

The LOC also requires a capital stock investment. In this example, a 25-basis-point stock requirement on a $25 million LOC would equal $62,500. That is a required investment, not an annual LOC fee, and any potential dividend impact is not reflected in this simplified earnings example. Members should evaluate the stock requirement separately as part of their overall FHLBank Boston capital stock position.

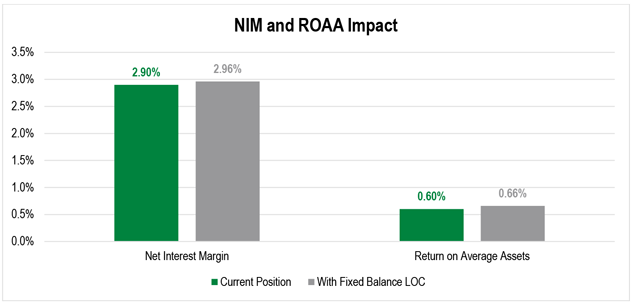

In this instance, net interest margin improves from 2.90% to 2.96%, and return on average assets improves from 0.60% to 0.66%.

These figures are illustrative only. Actual results will depend on the institution’s collateral position, LOC pricing, securities yields, loan yields, deposit pricing, tax position, capital strategy, liquidity policy, collateral availability, applicable collateral haircuts, and any other applicable fees. But the example highlights the broader point: the decision is not solely about securing public deposits but also about whether the institution’s collateral strategy aligns with its overall balance sheet strategy.

LOC Calculator

Members can use the Public Deposit LOC Strategy Calculator to go beyond the static examples shown above. The workbook includes live-updating charts, a redeployment yield sensitivity table, key output checks, and editable assumptions for pledged securities, available collateral capacity, remaining borrowing capacity, capital stock investment, LOC cost, and potential earnings impact.

Try the Public Deposit LOC Strategy Calculator.

For best results, download and open the calculator in the desktop version of Excel rather than Excel for the web, as some formulas, charts, or formatting may not function as intended in the browser version.

This calculator is for illustrative purposes only. It uses a Fixed Balance LOC example, so the fee and cost assumptions are specific. Members considering other public deposit LOC structures, including Variable Balance, Master Variable Balance, or Refundable Balance LOCs, may use the tool directionally by adjusting the LOC fee or expected annual cost assumption. Pricing, balance treatment, billing, refund, certification, and administrative requirements vary by product. The calculator assumes securities previously pledged to secure public deposits are released from that pledge and that the LOC is supported by existing eligible FHLBank Boston collateral capacity. Actual results will vary based on collateral availability, applicable collateral haircuts, LOC pricing, asset yields, deposit requirements, legal requirements, liquidity policy, capital stock position, and each member’s balance sheet strategy.

Where a FHLBank Boston LOC May Fit

An LOC may be worth evaluating when public deposits are meaningful to the funding mix, and securities are being pledged primarily to secure those balances. It may also be relevant when an institution wants to preserve liquidity flexibility, improve securities portfolio flexibility, or reduce operational friction tied to pledged securities.

Before replacing pledged securities with an LOC, institutions should evaluate both the economics and the operational fit. A few practical questions can help frame the review:

- How much of the securities portfolio is currently pledged to support public deposits?

- Are pledged securities limiting liquidity, investment, or ALM flexibility?

- What eligible collateral is available at FHLBank Boston to support the LOC?

- How would an LOC affect remaining borrowing capacity, capital stock requirements, and public deposit collateral coverage?

- Are there state, municipal, legal, policy, or depositor requirements that affect the structure?

The goal is to ensure the public deposit strategy aligns with the institution’s liquidity, earnings, collateral, and balance sheet objectives. For many institutions, the review should include finance, treasury, operations, legal, and relationship management.

LOCs as Part of Your Public Deposit Strategy

If your institution uses securities to secure public deposits, it may be worth reviewing whether that collateral approach still fits your liquidity, earnings, and balance sheet objectives. Members can use the LOC Calculator to test how different assumptions may affect pledged securities, available FHLBank Boston collateral capacity, remaining borrowing capacity, capital stock investment, LOC cost, and potential earnings impact. Please contact me at tyler.buckeridge@fhlbboston.com, or reach out to your relationship manager for more details.

FHLBank Boston does not act as a financial advisor, and members should independently evaluate the suitability and risks of all advances. The content of this article is provided free of charge and is intended for general informational purposes only. FHLBank Boston does not guarantee the accuracy of third-party information displayed in this article, the views expressed herein do not necessarily represent the view of FHLBank Boston or its management, and members should independently evaluate the suitability and risks of all advances.

Forward-looking statements: This article uses forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 and is based on our expectations as of the date hereof. All statements, other than statements of historical fact, are “forward-looking statements,” including any statements of the plans, strategies, and objectives for future operations; any statement of belief; and any statements of assumptions underlying any of the foregoing. The words “expects”, “may”, “likely”, “continue”, “possible”, “to be”, “will,” and similar statements and their negative forms may be used in this article to identify some, but not all, of such forward-looking statements. The Bank cautions that, by their nature, forward-looking statements involve risks and uncertainties, including, but not limited to, the uncertainty relating to the timing and extent of FOMC market actions and communications and economic conditions (including effects on, among other things, interest rates and yield curves). The Bank reserves the right to change its plans for any programs for any reason, including but not limited to legislative or regulatory changes, changes in membership, or changes at the discretion of the board of directors. Accordingly, the Bank cautions that actual results could differ materially from those expressed or implied in these forward-looking statements, and you are cautioned not to place undue reliance on such statements. The Bank does not undertake to update any forward-looking statement herein, or that may be made from time to time on behalf of the Bank.

As a sales & strategies specialist, Tyler applies his analytical skills and data-driven insights to support FHLBank Boston members and enhance their understanding of how the Bank’s products and services can help them achieve their performance goals.