Strategic Implications of Commercial Real Estate Loan Repricing Wave

Tyler Buckeridge

Over the next two years, commercial real estate (CRE) loans originated from 2020 through 2022 will reprice into a very different rate and macro environment. How that repricing wave affects debt-service coverage ratios (DSCRs), valuations, earnings, and capital, and putting the right credit, liquidity, and funding strategies in place – including leveraging FHLBank Boston products – while the planning window is still open is crucial.

The Repricing Wave: Timing and Scale

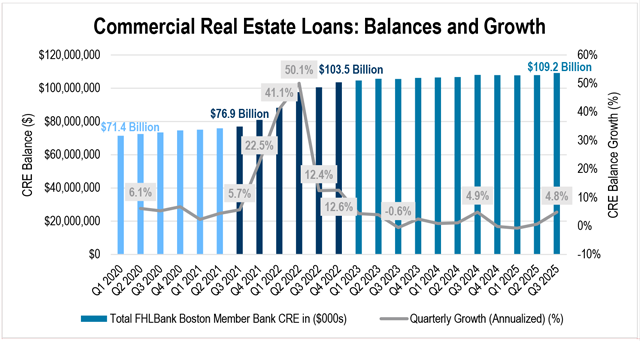

Since 2020, member CRE portfolios have followed a clear three-stage pattern: ramp, surge, and plateau.

In the initial ramp phase from Q1 2020 through Q2 2021, balances grew by about $4.48 billion, roughly a 5% annualized Compound Annual Growth Rate, as banks and credit unions steadily added CRE at low yields. That was followed by a much more aggressive surge from Q3 2021 through Q4 20222 when portfolios expanded by another $26.62 billion at an annualized growth rate of nearly 27%. Since then, growth plateaued from Q1 2023 through Q3 2025, adding about $4.51 billion in CRE at a muted annualized pace of about 1.6%.

Since income-producing CRE is often structured with a five-year repricing, these three vintages roll forward into a matching ramp–surge–plateau maturity profile. The early 2020–2021 ramp translates into a late 2025–early 2026 refinancing wave, while the far larger 2021–2022 surge becomes a late-2026 to 2027 maturity crest.

Possible Repricing Scenarios: Soft vs. Hard Landings

The next cycle may be driven less by a single Federal Reserve forecast and more by the range of possible easing paths and macro landings. Thinking in terms of the three scenarios outlined below helps frame how different combinations of rate cuts and economic conditions could shape refinancing behavior, borrower performance, margins, and ultimately capital and balance-sheet resilience.

| Scenario A | Scenario B | Scenario C | |

| Aggressive Easing | Moderate Landing | Higher for Longer | |

| Macro Environment | Slower growth leads the Fed to cut rates more quickly. | Growth slows, but a prolonged recession is avoided. | Growth remains and/or inflation is persistent. |

| Borrower Credit | Loans refinance into rates closer to 2020-2021 levels, so DSCR pressure may be limited. | Loans reprice 100-200 higher, creating more watchlist names and restructurings. | Loans reprice much higher, leading to pressure on DSCR and valuations. |

| Earnings Impact | NIM pressure due to asset repricing, plus potential higher credit costs. | Asset yields remain strong, but pressure from credit deterioration builds. | Life from asset yields offset by funding costs and asset quality issues. |

Across all three landing paths, a common theme is that a large share of the 2020–2022 vintage may refinance with less DSCR cushion than it started with, in an environment where funding is more expensive and supervisory focus on CRE is sharper.

Why DSCR Matters So Much

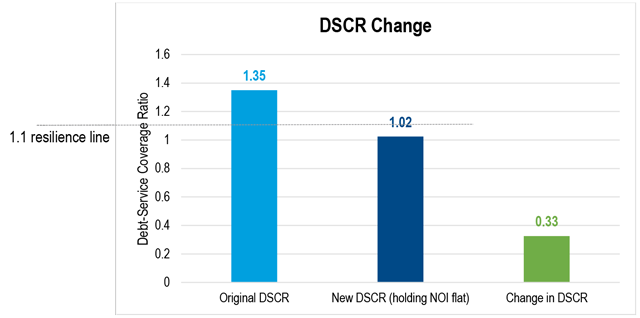

These macro paths can appear on the balance sheet through DSCR compression on refinancing loans. DSCR cushions may thin out when debt service resets well above origination levels. Once that cushion narrows, otherwise stable properties become more sensitive to small shocks in values, vacancies, or operating expenses. Regulators and investors often flag 1.10x DSCR as the line between resilient and vulnerable. Many 2020–2021 originations that started around 1.30–1.45× could reset closer to 1.05x–1.00x at today’s refinancing rates.

A practical way to prepare for the 2025–2027 repricing wave is to align three things: credit risk management, funding strategy, and liquidity and ALCO planning.

Consider a $10 million suburban office loan, 25-year amortization, 5-year term, underwritten at a 3.50% coupon and 1.35× DSCR. When that loan reprices into the mid-6% range (e.g., 6.25%), annual debt service jumps roughly 30% to 35%. Holding net operating income flat to isolate the rate effect, DSCR falls to roughly 1.02×, shrinking the cash-flow cushion from about 35% to only a few percentage points.

Strategies for Members

A practical way to prepare for the 2025–2027 repricing wave is to align three things: credit risk management, funding strategy, and liquidity and ALCO planning.

- Credit Risk Management – Goal: Use DSCR to decide where to spend time first

- Stress test CRE books against multiple rates and macro paths and observe DSCR and valuation impacts by segment.

- Flag exposures where DSCR drops near or below 1.10x, especially in office, hospitality, and challenged retail.

- Build playbooks for at-risk borrowers that include rate structure changes, amortization tweaks, additional equity, partial paydowns, or collateral support. Engage borrowers early, while DSCR is compressing—not after it has failed.

- Funding Strategy – Goal: Decide how to pay for the wave before it hits

- Forward-Starting Advances: Lock in rates today while easing expectations are priced in, with draws timed to the 2026–2027 maturity wall. Forward Starting Advances can be structured as bullets or amortizing advances, allowing funding to track CRE cash flows more closely.

- Amortizing Advances: Pair amortizing advances with long-dated amortizing CRE loans to reduce maturity mismatch and hedge against extension pressures if borrowers need more time at reset.

- Short and Intermediate Classic Advances: With the current curve already embedding meaningful near-term easing, locking a one- to two-year Classic Advance now secures that forward-implied value. Unless there is a strong conviction that the cutting cycle will be materially deeper and faster than markets expect, terming out near-dated funding helps preserve cost certainty and reduces reliance on promo CDs when refinancing demand peaks.

- Liquidity & ALCO Planning – Goal: Line up cash flows and capacity around the CRE maturity wall

- Align investment roll-off with expected CRE maturities: Use upcoming investment cash flows (calls, maturities, prepayments) to naturally fund parts of the repricing wave, rather than having everything hit at once.

- Optimize borrowing capacity through collateral management: Work with the FHLBank Boston collateral team to review pledged and unpledged collateral, refresh valuations, and add CRE loans and other eligible collateral. Ensuring sufficient, well-structured collateral in advance can expand available capacity and make it easier to draw term funding when the 2025–2027 maturity wall arrives.

- Use advances to bridge timing gaps: Where loan repricing, deposit behavior, and investment runoff do not align, use Classic and Amortizing Advances as a bridge rather than relying solely on short-term, potentially volatile funding sources.

- Make the CRE maturity wall a standing ALCO agenda item: Bring together the credit, lending, treasury, and liquidity teams around a shared view of the 2026–2027 wall – what is maturing, how it is likely to reprice, what is the funding plan, and where contingency capacity sits.

The Bottom Line

The upcoming repricing wave isn’t a “risk event” to avoid. It’s an inevitable refinancing cycle. For some depositories, it will be a margin opportunity, and for others, a credit headwind.

Members that triage DSCR risk early, collaborate proactively with borrowers, pre-position term funding, and align liquidity and ALCO planning with the CRE maturity wall can navigate this wave from a position of strength. FHLBank Boston’s strategies team is ready to work with you to map credit, funding, and liquidity tools to your specific repricing schedule, helping you capture the value of today’s market expectations while protecting against tomorrow’s uncertainty.

Flexible Funding for the CRE Repricing Wave

The CRE maturity wall will test how well funding, liquidity, and collateral are aligned to your balance sheet. FHLBank Boston’s Financial Strategies group can help you model the impact of different rate paths, structure an advance strategy, and optimize collateral to support your plan.

Please contact me at tyler.buckeridge@fhlbboston.com or reach out to your relationship manager for more details.

FHLBank Boston does not act as a financial advisor, and members should independently evaluate the suitability and risks of all advances. The content of this article is provided free of charge and is intended for general informational purposes only. FHLBank Boston does not guarantee the accuracy of third-party information displayed in this article, the views expressed herein do not necessarily represent the view of FHLBank Boston or its management, and members should independently evaluate the suitability and risks of all advances.

Forward-looking statements: This article uses forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 and is based on our expectations as of the date hereof. All statements, other than statements of historical fact, are “forward-looking statements,” including any statements of the plans, strategies, and objectives for future operations; any statement of belief; and any statements of assumptions underlying any of the foregoing. The words “expects”, “may”, “likely”, “continue”, “possible”, “to be”, “will,” and similar statements and their negative forms may be used in this article to identify some, but not all, of such forward-looking statements. The Bank cautions that, by their nature, forward-looking statements involve risks and uncertainties, including, but not limited to, the uncertainty relating to the timing and extent of FOMC market actions and communications and economic conditions (including effects on, among other things, interest rates and yield curves). The Bank reserves the right to change its plans for any programs for any reason, including but not limited to legislative or regulatory changes, changes in membership, or changes at the discretion of the board of directors. Accordingly, the Bank cautions that actual results could differ materially from those expressed or implied in these forward-looking statements, and you are cautioned not to place undue reliance on such statements. The Bank does not undertake to update any forward-looking statement herein, or that may be made from time to time on behalf of the Bank.

As a Sales & Strategies Specialist, Tyler applies his analytical skills and data-driven insights to support FHLBank Boston members and enhance their understanding of how the Bank’s products and services can help them achieve their performance goals.