Advance Solutions for Different Rate Scenarios

Andrew Paolillo

With uncertainty surrounding the near-term path of interest rates, several funding strategies can be used to benefit from the changes in the yield curve.

Hikes, Pauses or Cuts

The rate hiking cycle of 2022-23 caught many market participants and prognosticators off-guard, as the quickness and magnitude of the monetary tightening were so different from what was experienced in the Great Financial Crisis. But with overnight rates now above 5%, there are more questions than answers about what is next. Will fighting inflation remain job number one, and will the hikes continue? Will the Fed pause and wait? Will factors such as the banking industry turmoil necessitate a sharp pivot to rate cuts?

An interesting dynamic is currently at play, as market-implied expectations on the path of short-term rates differ markedly from what the Federal Reserve has communicated publicly. It’s been said that the fixed-income markets tend to view the world in a “glass half-empty” perspective, and the depth and persistence of inverted yield curves imply that many expect rates to come down soon and sharply.

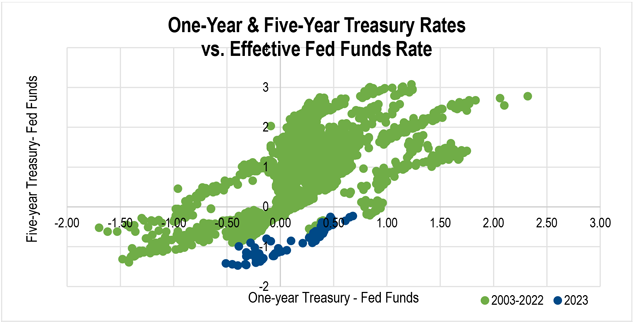

As the chart below shows, the yield curve’s slope is deeply inverted. The one-year and five-year Treasury compared to Fed Funds spreads are both negative, with the five-year currently persisting at the most inverted levels over the last 20 years. Other market-implied metrics also signal that the market is positioning for a quick and aggressive pivot to an easing cycle.

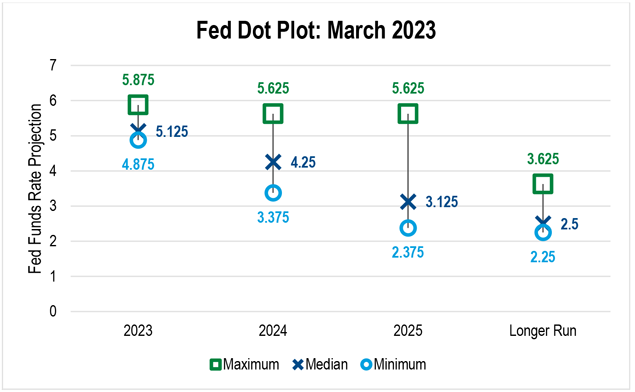

However, the Federal Reserve indicates that the trajectory of interest rates may take a smoother path. In the most recently released (March 2023) “Dot Plot” of future rate expectations, the median projection from the survey of Fed governors forecasts the Fed Funds rate to be at 5.125% at year-end 2023, implying a long pause given that 5.125% was the level hit with the 25 basis point hike at the May 2023 meeting.

Funding that Aligns with the Big Picture

So with the Fed and the market not quite in alignment on where short rates will go next, what are the implications for FHLBank Boston members as it relates to their approach to the positioning and use of wholesale funding? Below we will identify some borrowing strategies that may serve members well in scenarios where the Fed hikes, pauses or cuts rates.

Scenario 1: The Fed Continues Hiking Rates

March 2023 was a tumultuous time for the banking industry but, as quickly as things escalated – driven by troubles at a handful of large banks – conditions stabilized rapidly shortly thereafter. Within a month, equity markets returned to pre-March levels, and the Fed initiated a rate hike of 25 basis points just weeks after banks controlling more than $300 billion in aggregate assets were taken over by the FDIC. If the Fed deems that the economy and markets are sufficiently strong, and the work to tame inflation is not yet done, then “higher for longer” may be how the situation plays out.

Given that the current shape of the yield curve is highly discounting this potential path of rates, this may present an opportunity in longer-term fixed-rate funding. And given changing assumptions on their deposit portfolio as growth and retention have become difficult, many depository members have found themselves more liability sensitive than they have historically been. Accordingly, activity in long-term fixed-rate advances from FHLBank Boston depository members has been robust over the last few quarters.

The Fed may get to a place where they believe further tightening is not warranted, but conditions are not yet to a point where a shift to a more accommodative stance is appropriate.

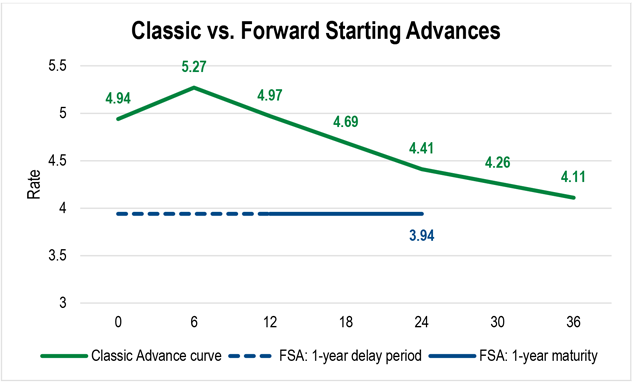

In a recent case study, we looked at how the Symmetrical Prepayment Advance is very similar to the Classic Advance in that it hedges interest-rate and liquidity risk, but with the added potential of being able to capture a gain in a rising-rate environment – much like how one can sell a bond at a gain in a falling-rate environment. Another strategy that may be beneficial in this scenario would be using the Forward Starting Advance. This advance allows members to lock in a rate based on today’s yield curve but delay the funds’ disbursement for up to two years. The chart below shows that the inverted yield curve creates a situation where forward rates are below spot rates. This can be a useful way to “pre-replace” high-cost certificates of deposit initiated in 2023 as deposit betas and competition for funding accelerated. Here we’ve highlighted a Forward Starting Advance with a delay of one year that then disburses to become a one-year Classic Advance at 3.94%. This compares favorably to immediately disbursed one-year and two-year Classic Advances 50 to 100 basis points higher.

Scenario 2: The Fed Stops Hiking but Pauses for A While

The Fed may get to a place where they believe further tightening is not warranted, but conditions are not yet to a point where a shift to a more accommodative stance is appropriate. For much of 2022 and through the first half of 2023, interest-rate volatility was at or near historic highs, driven by uncertainty about what action the Fed would take next. In the scenario where the Fed neither hikes nor cuts for a sustained period, it will likely be beneficial to balance sheet decisions that favor enhanced current income versus approaches reliant on big changes in the direction of rates. On the asset side of the balance sheet, one way to express this view is by holding mortgage loans or mortgage-backed securities, where the excess spread is earned due to taking prepayment risk. A similar solution exists on the liability side – the HLB-Option Advance.

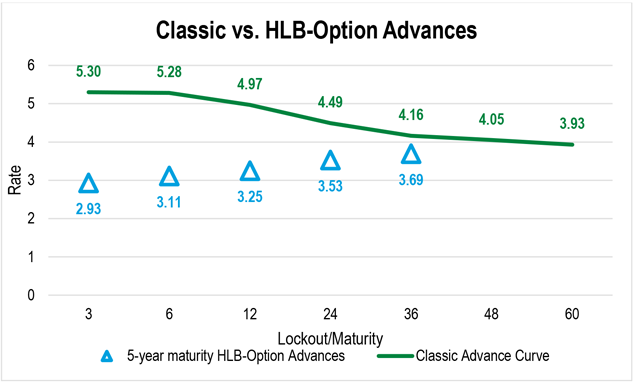

The HLB-Option Advance is a popular funding tool with members, especially in this environment with an inverted yield curve and elevated interest-rate volatility. Granting FHLBank Boston the right to put the advance back at pre-determined intervals after a defined lockout period allows for funding rates lower than comparable term Classic Advances. As discussed in a recent webinar, these types of advance structures can be useful in providing immediate margin relief, a top concern for many in 2023, as deposit costs rise and asset yields slowly reprice higher.

Scenario 3: The Fed Pivots to Rate Cuts

If rate cuts materialize sooner rather than later, it’s intuitive that a shorter repricing frequency on funding would be a favorable feature to have. A three-month advance that matures right after a rate cut is likely to outperform a longer advance. However, even when comparing strategies with the same average life, there can be differences in current total funding cost and the ability to improve that cost if rates drop.

Below we compare three different approaches, all using Classic Advances and the Daily Cash Manager Advance that produce a six-month average life, a six-month bullet, a barbell using an overnight borrowing and a 12-month advance, and a ladder of overnight borrowings plus advances every three months. If one desired to have the most flexibility in down-rate scenarios, both to reprice lower but also potentially reduce the amount of funding needed, then the barbell, followed by the ladder approach, would provide that, as they have 40-50% of maturities coming due within the next three months. On top of more near-term maturities, the barbell also has a lower day-one cost than the other two strategies. That heavy allocation to the very front end presents a possible risk from spread widening and further rising rate pressures, but the initial cost savings help to mitigate that. Ultimately, the strategy aligns with the bigger picture balance sheet decision to target benefits from rate cuts.

Flexible Funding

Recent market conditions have created challenges and opportunities for FHLBank Boston members. Our Financial Strategies group has developed a suite of analytical tools designed to help you identify the funding solutions that best fit the unique needs of your balance sheet. Please contact me at 617-292-9644 or andrew.paolillo@fhlbboston.com or reach out to your relationship manager for more details.

FHLBank Boston does not act as a financial advisor, and members should independently evaluate the suitability and risks of all advances. The content of this article is provided free of charge and is intended for general informational purposes only. FHLBank Boston does not guarantee the accuracy of third-party information displayed in this article, the views expressed herein do not necessarily represent the view of FHLBank Boston or its management, and members should independently evaluate the suitability and risks of all advances. Forward-looking statements: This article uses forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 and is based on our expectations as of the date hereof. All statements, other than statements of historical fact, are “forward-looking statements,” including any statements of the plans, strategies, and objectives for future operations; any statement of belief; and any statements of assumptions underlying any of the foregoing.. The words “expects”, “may”, “likely”, “could”, “to be”, “will,” and similar statements and their negative forms may be used in this article to identify some, but not all, of such forward-looking statements. The Bank cautions that, by their nature, forward-looking statements involve risks and uncertainties, including, but not limited to, the uncertainty relating to the timing and extent of FOMC market actions and communications; economic conditions (including effects on, among other things, interest rates and yield curves); and changes in demand and pricing for advances or consolidated obligations of the Bank or the Federal Home Loan Bank system. The Bank reserves the right to change its plans for any programs for any reason, including but not limited to legislative or regulatory changes, changes in membership, or changes at the discretion of the board of directors. Accordingly, the Bank cautions that actual results could differ materially from those expressed or implied in these forward-looking statements, and you are cautioned not to place undue reliance on such statements. The Bank does not undertake to update any forward-looking statement herein or that may be made from time to time on behalf of the Bank.

As vice president, director of member strategies and solutions at FHLBank Boston, Andrew leads the Strategy team in creating customized funding strategies for members.